In this article, I’ll share what purchase order financing is, how and when you should use it, and the potential pros and cons.

Table of Contents

- What is purchase order financing?

- Who needs purchase order financing?

- How much does purchase order financing cost?

- The Pros of Purchase Order Financing

- The Cons of Purchase Order Financing

- How does purchase order financing work? [Template]

- PO Financing Companies to Consider

- How to Choose the Right PO Financing Company

- Getting Started

What is purchase order financing?

Purchase order financing allows businesses to finance goods necessary for production from their suppliers before receiving payment from a customer. The advanced funds can only be used to purchase goods supporting the customer’s order.

Purchase orders are legal documents issued by buyers communicating the intent to purchase goods from a company. If the company selling the goods does not have the inventory to fulfill the order or purchase materials from their supplier, the purchase order can be used to apply for advance funding paid to the supplier to support the fulfillment of the order.

Who needs purchase order financing?

Purchase order financing helps businesses bridge the gap between large customer orders and supplier payments. It’s particularly valuable for:

- Manufacturing companies handling custom orders.

- Import/export businesses managing international shipments.

- Wholesale distributors scaling their operations.

- Seasonal businesses managing demand spikes.

- Startups and growing companies that haven’t built extensive credit history.

For many businesses, traditional funding options may be out of reach or too slow to capture time-sensitive opportunities. PO financing enables them to take on more orders and fuel sustainable growth.

Free Sales Plan Template

Outline your company's sales strategy in one simple, coherent sales plan.

- Target Market

- Prospecting Strategy

- Budget

- Goals

Download Free

All fields are required.

Form not available

How much does purchase order financing cost?

Purchase order financing typically costs between 1% to 6% of the supplier’s monthly costs, based on factors like your company’s financial health and order size. Here’s what shapes your rate:

- Order amount. Larger orders (over $500,000) often qualify for lower rates since the financing company can spread their risk.

- Customer creditworthiness. A Fortune 500 buyer means less risk than a smaller company, potentially reducing your rate.

- Time to payment. The longer it takes your customer to pay, the more you pay in fees. Most PO financing companies charge in 30-day blocks.

- Supplier relationships. Strong supplier ties can help reduce costs since they may offer better payment terms.

For example, if you get a $100,000 purchase order with net-30 terms, you might pay between $1,800 and $6,000 in fees. That’s steeper than traditional bank loans, but remember — you’re paying for speed and accessibility.

Most PO financiers structure payments as a flat monthly fee rather than an annual percentage rate (APR). This makes it easier to calculate your total costs upfront and decide if the math works for your margins.

The Pros of Purchase Order Financing

No Personal Credit Requirements

When I talk to fellow founders about purchase order financing, this is often their biggest relief: Your personal credit score doesn’t make or break the deal.

Unlike traditional bank loans where they dig through your credit history, PO financiers care more about your customer’s ability to pay than yours.

I’ve seen this work especially well for immigrant founders and entrepreneurs who haven’t built up their credit yet. One founder I worked with had a stellar product and a purchase order from a Fortune 500 company but no credit history in the U.S.

The financier looked at his customer’s strong payment history and approved the deal within days. Your business opportunity matters more than your FICO score here.

Quick Access to Capital

Most businesses get their funds within 5-10 business days after approval, which beats the months-long wait for traditional financing.

The streamlined process helps you move fast when big opportunities come around. Your customer submits a purchase order, you send it to the financier, and they review it — often giving initial feedback within 24-48 hours.

Many PO financing companies have digital platforms where you can upload documents and track the approval process in real time. This means no scheduling multiple bank meetings or gathering years of financial statements.

Some companies even integrate with finance CRM platforms like HubSpot to streamline the entire process, from initial application to final payment tracking.

The speed makes a real difference when suppliers need upfront payments or when you’re racing against tight delivery deadlines. Even complex deals typically close within two weeks.

Maintains Equity Ownership

PO financing lets you keep 100% ownership of your business while accessing the capital you need to grow.

Unlike equity financing, where you give up a piece of your company, PO financing is purely transactional. You pay a fee for the service, then move on with full control of your business.

For perspective, most early-stage equity rounds dilute founders by 15-25% per round. That adds up fast when you need multiple rounds to fund your growth. But with PO financing, whether you use it once or a hundred times, your cap table stays clean.

This matters most when you’re scaling quickly and want to maintain decision-making power over your company’s direction.

Scales With Your Orders

The financing amount automatically adjusts based on your purchase orders. When orders are small, you borrow less. When they grow, your funding grows, too.

Most PO financing companies work with orders ranging from $50,000 to over $10 million. This flexibility means you’re never locked into borrowing more than you need for each deal.

The scalability works both ways — you can use it for a single large order or set up a revolving facility for multiple orders. One month, you might finance a $75,000 order, and the next month, you might finance a $500,000 one. Your available funding adapts to your actual sales pipeline.

This natural scaling helps you manage cash flow without overextending your business.

No Hard Assets Required

Traditional lenders want to see buildings, equipment, or inventory as collateral. PO financing takes a different approach — your purchase order is the asset.

The financier looks at the strength of your customer’s promise to pay rather than the physical assets on your balance sheet. This works particularly well for service businesses or companies with light asset models.

Even businesses operating from home offices or co-working spaces can qualify. Your customer’s purchase order and creditworthiness serve as the main security.

This removes one of the biggest barriers newer businesses face when seeking capital. You can access substantial funding without pledging personal assets or business equipment as collateral.

Free Sales Plan Template

Outline your company's sales strategy in one simple, coherent sales plan.

- Target Market

- Prospecting Strategy

- Budget

- Goals

Download Free

All fields are required.

Form not available

The Cons of Purchase Order Financing

Supplier Verification Required

Your suppliers need to pass the financier’s verification process. This means sharing their business details and sometimes agreeing to specific payment terms.

Some suppliers feel uncomfortable with this level of scrutiny or prefer not to deal with third-party financiers. Others might raise their prices to cover the additional paperwork and coordination.

This verification process can strain relationships with suppliers who value their privacy or prefer simpler transactions. You’ll need backup suppliers ready in case your preferred ones don’t want to participate.

Higher Costs Than Traditional Loans

Monthly fees of 1.8% to 6% might seem reasonable for a single order, but they add up when annualized. A rate that works out to 24-72% APR means you need healthy profit margins to absorb these costs.

Most traditional bank loans or lines of credit charge 5-15% annually. But here’s the reality check — PO financing serves a different purpose. You’re paying for speed and accessibility, not just the money.

Consider these costs as part of your overall pricing strategy. If fulfilling larger orders helps you negotiate better supplier rates or reach economies of scale, the math might still work in your favor.

Customer Relationship Impact

Your customer learns about the financing arrangement since they’ll need to verify the purchase order and agree to pay the finance company directly.

Some customers view this as a red flag about your financial stability. Others might hesitate to share their financial information with a third party.

Managing these conversations requires careful communication. You need to frame PO financing as a strategic tool for growth rather than a last resort for cash flow problems.

How does purchase order financing work? [Template]

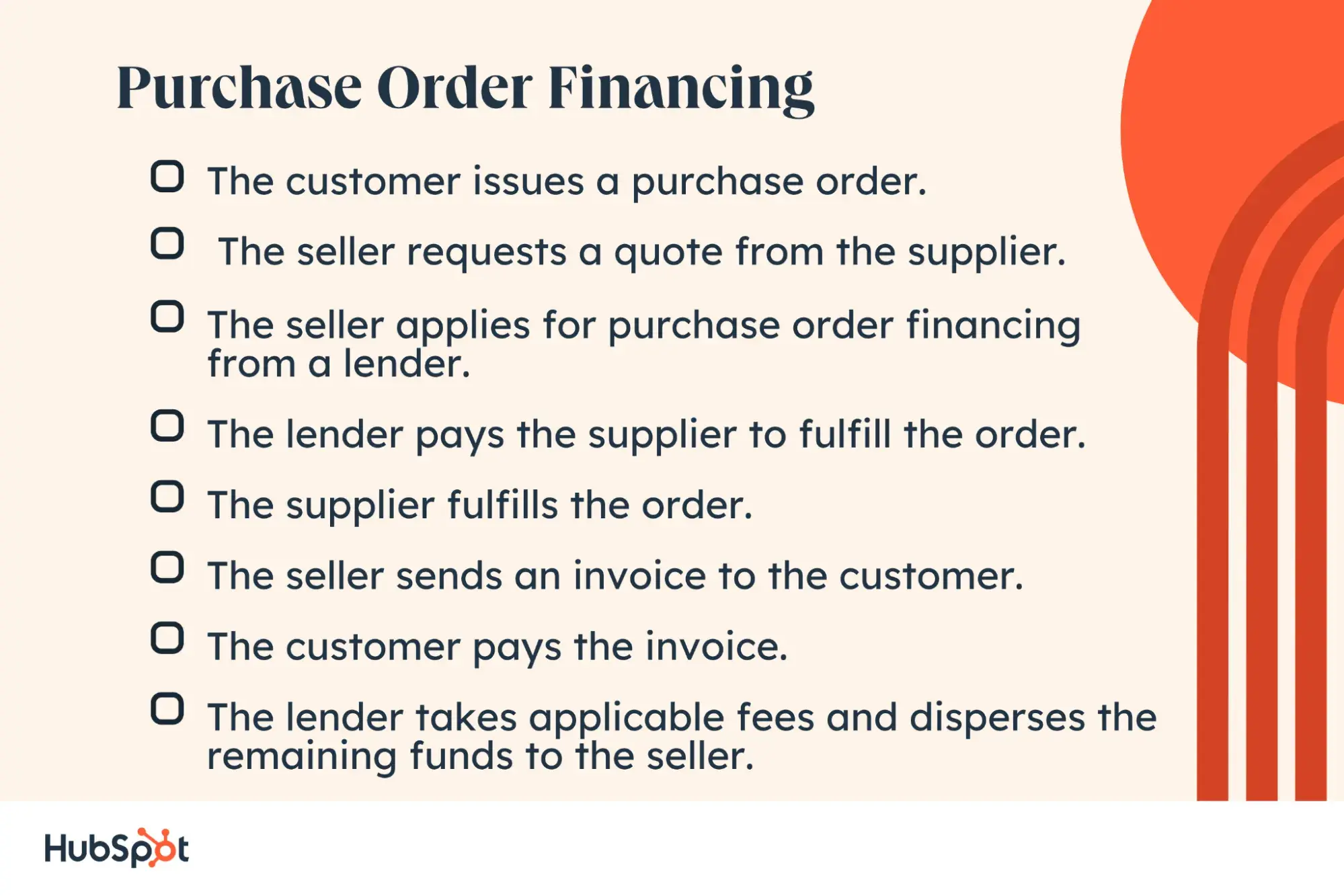

There are typically four parties involved in purchase order financing transactions. They are:

- Seller/borrower. The company that needs financing to fulfill the customer’s order.

- Lender. This company finances the transaction. They review the purchase order and borrower’s qualifications to disperse funds directly to the supplier to fulfill the order at hand.

- Supplier. This party provides the goods or materials needed to fulfill the order. They receive initial funds directly from the lender.

- Customer. The customer provided the initial purchase order requesting goods from the borrower’s company. They receive the final product delivered by financing. Their payment typically goes directly to the lender.

Now that we understand who is involved in a purchase order financing deal, I’ll walk you through the steps it takes to complete this type of order.

1. The customer issues a purchase order.

To begin the process, a customer sends a purchase order to a seller with the intention of making a purchase. The purchase order specifies the product, the number of units, and the date they would like to receive the order by.

For example, if an office manager decides to upgrade the furniture in their office building and wants to purchase 100 new office chairs, they can start by drafting a purchase order and sending it to the furniture company they would like to order from. The purchase order should indicate the specific chair they would like to order, the number of chairs (in this case, 100), the delivery address, and the date they would like to receive the chairs.

2. The seller requests a quote from the supplier.

Once the seller receives the purchase order, they can share the purchase order information with the supplier. The supplier determines if they have the inventory to fulfill the order and sends the seller a quote outlining how much it will cost to fulfill the order.

Once the seller has this information, they can determine if they have the cash on hand to make the purchase from the supplier upfront, or they can decide to pursue purchase order financing to pay the supplier.

Continuing the example above, when the office furniture company goes to their supplier to price the order of 100 chairs, they realize they did not have access to enough funds to purchase the chairs from the supplier. They decide to pursue purchase order financing to provide the chairs to the customer.

3. The seller applies for purchase order financing from a lender.

Once the seller decides to pursue purchase order financing, they must apply for the funds needed from a financing company. The customer’s initial purchase order and the quote from the supplier must be provided to be considered for funding.

In the case of the office furniture, the furniture company applies for funds from a financing company. After reviewing the initial purchase order and the supplier quote, the lender approves the seller’s application and agrees to finance this effort.

4. The lender pays the supplier to fulfill the order.

After the seller has been approved, the lender provides the necessary funds to the supplier directly. This amount should cover the cost of manufacturing and delivering the goods requested in the purchase order.

5. The supplier fulfills the order.

Once the supplier receives the funds from the lender, they provide the products outlined by the original purchase order and deliver the goods directly to the customer. The seller is typically not involved in this step.

For example, when the furniture supplier makes and ships the 100 chairs, they send the order directly to the office manager who provided the initial purchase order. The office furniture company does not serve as a middleman during this step of the process.

6. The seller sends an invoice to the customer.

After the supplier delivers the order, the seller sends an invoice to the customer requesting payment. The payment terms outlined in the invoice should adhere to the terms outlined by the lender when they provided the initial funding.

7. The customer pays the invoice.

When the customer pays the invoice, their funds go directly to the financing lender.

Again, during this step of the process, the furniture company does not serve as a middleman. The office manager will pay the financing lender directly.

8. The lender takes applicable fees and disperses the remaining funds to the seller.

Once the lender receives the funds from the customer, they take any applicable fees as outlined in their original lending agreement and give the remaining funds to the seller.

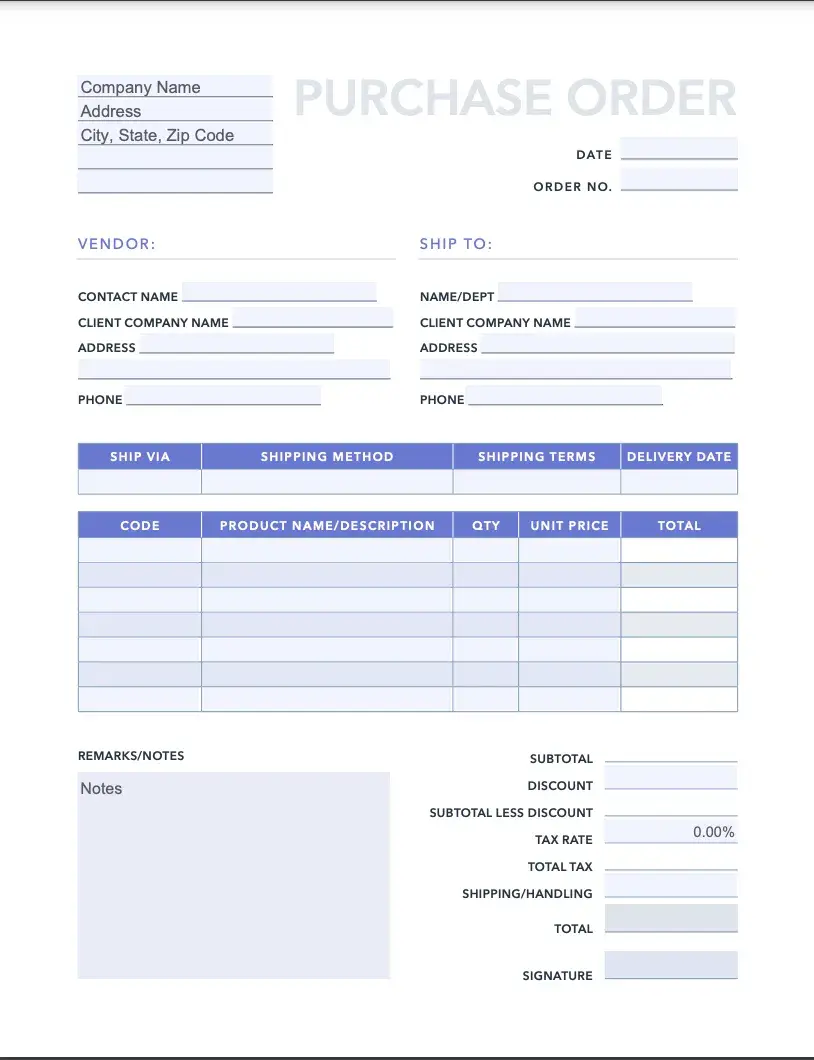

Here’s a purchase order template that can be used for this process:

Download our easy-to-use purchase order template.

Free Sales Plan Template

Outline your company's sales strategy in one simple, coherent sales plan.

- Target Market

- Prospecting Strategy

- Budget

- Goals

Download Free

All fields are required.

Form not available

PO Financing Companies to Consider

Finding a reliable PO financing partner requires looking beyond interest rates and minimum funding amounts. Here’s a breakdown of the top companies in this space, along with their specialties and ideal customer profiles.

SMB Compass

SMB Compass specializes in smaller PO deals starting at $10,000 — notably lower than most competitors’ $50,000 minimum. The average interest rate is 7.99% APR.

Their digital portal lets you monitor the entire funding process, from initial submission to supplier payments. Most clients receive term sheets within 24 hours of applying.

They offer nine types of business loads and are accessible to a variety of borrowers.

Best for: Businesses operating for over two years and with strong personal credit scores.

Liquid Capital

Liquid Capital processes purchase orders ranging from $20,000 to $20 million, with typical approval times of 24 hours. They serve clients across North America.

Their repayment terms typically run up to 90 days, and the estimated fees per 30 days are 2-4%.

Best for: Mid-sized businesses in various industries ranging from chemicals and plastics to medical ales.

Southstar Capital

Southstar Capital has experience in government and business contracts and their processing time averages 2-5 days. They also base their credit decisions on your customer’s credit.

They offer some of the most flexible repayment terms, and you can also combine PO financing with receivable financing for accounts.

Best for: Companies seeking other forms of financing complementary to PO financing.

AdvancePoint

AdvancePoint handles purchase orders for new businesses with financing up to $500,000, with a focus on technology hardware and software resellers. They complete due diligence in 2-10 business days.

AdvancePoint also offers a variety of other financing options, including equipment financing and bad credit business loans.

Best for: Small to mid-sized businesses who want to compare multiple loan options.

How to Choose the Right PO Financing Company

The right PO financing partner can mean the difference between steady growth and missed opportunities. I believe these five factors will help you evaluate which company best matches your business needs, industry requirements, and operational style.

1. Evaluate their supplier relationship management.

A PO financing company’s reputation with suppliers can directly impact your deal terms. When evaluating potential financiers, look beyond their funding capabilities to their supplier network and relationship management approach.

Behrouz Bakhtiari, a supply chain expert at McMaster University, points out an often-overlooked benefit:

“Companies may be surprised to find out that suppliers are willing to provide better terms if a PO lender is involved in the transaction. If a reputable PO lender is involved, suppliers will become less risk averse in their price and terms proposals.” This means choosing the right PO financing partner could help you secure more favorable supplier terms.

Ask potential financiers about their supplier onboarding process and communication protocols. The best companies maintain strong relationships across various industries and can provide references from their current supplier network.

I suggest you request to speak with suppliers they’ve worked with previously. Their experiences will tell you more about the financier’s reliability than any sales pitch.

2. Assess their seasonal business experience.

When choosing a PO financing partner for seasonal business needs, look closely at their track record with similar cyclical industries. The right partner should understand the unique challenges of seasonal demand.

As Bakhtiari notes, “Suppliers providing seasonal items often work with numerous customers, and the number of orders tends to increase rapidly before the season starts. This may place unforeseen strains on the supplier, resulting in delayed shipments.”

Ask potential financiers specific questions about their seasonal business protocols:

- How do they handle supplier delays during peak seasons?

- What contingency plans do they have for shipping disruptions?

- Can they provide examples of successful seasonal business financing?

The best PO financing companies have systems to manage seasonal complexities and can demonstrate past success with similar business cycles.

3. Consider their international capabilities.

Your PO financing partner needs expertise in international trade regulations and financing structures for businesses operating across borders. Each country has its own set of rules and requirements.

Bakhtiari highlights a crucial consideration, “One area is different terms and requirements for factoring in different countries. The PO lender and factoring agencies in different countries may employ different terms and conditions.”

When evaluating international capabilities, verify:

- Their experience with your target markets.

- Their network of international banking relationships.

- Their understanding of currency exchange risks.

- Their track record with cross-border transactions.

I recommend looking for partners who can clearly document their international processes and have established relationships with reliable factoring agencies in your key markets.

4. Review their risk management approach.

A purchase order financing partner’s approach to risk tells you a lot about their reliability and fit for your business. Their risk assessment process should be thorough but not overly restrictive.

Bakhtiari emphasizes this balance, “PO financing needs to be used only when other options are unavailable or do not provide sufficient funding. It’s a great option when traditional options do not provide timely or sufficient funding, and there’s an opportunity for growth and market share acquisition.”

Look for partners who:

- Have clear criteria for evaluating orders.

- Provide transparent risk assessment processes.

- Can explain their approval requirements upfront.

- Show flexibility based on customer creditworthiness.

Ask about their risk mitigation strategies and how they handle common challenges like shipping delays or supplier issues. Their answers reveal how they’ll respond when problems arise.

5. Check their shipping timeline policies.

Shipping delays can quickly turn a profitable order into a loss when using PO financing. You need a partner whose policies protect your margins when timelines slip.

Bakhtiari warns about this critical risk:

“If a supplier does not commit to the planned shipping timeline, the additional PO financing costs can easily eat into the profit margins of the transaction. Even though there may be penalties for delayed shipments charged to the supplier, these often prove to be less than the additional cost charged by the PO lender.”

When evaluating potential partners, ask:

- How they handle supplier shipping delays.

- What additional fees apply when shipments run late.

- Whether they offer flexibility on payment terms for delayed orders.

I think the best partners have clear policies that align supplier penalties with their late fees to protect your bottom line.

Getting Started

Successful PO financing often comes down to relationship management more than pure financials. The companies that get the best terms aren’t necessarily the ones with the strongest balance sheets but those who build solid relationships with their financiers, suppliers, and customers.

The most valuable insight? The importance of running the numbers before you need them. Understanding your margins and calculating potential financing costs ahead of time puts you in a much stronger position when that big order finally lands on your desk.

Free Sales Plan Template

Outline your company's sales strategy in one simple, coherent sales plan.

- Target Market

- Prospecting Strategy

- Budget

- Goals

Download Free

All fields are required.

Form not available

Accounting

![Debt-to-Equity Ratio, Demystified [+Helpful Formulas]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/debt-to-equity-1-20250115-1477462.webp)