.png?width=112&height=112&name=Image%20Hackathon%20%E2%80%93%20Horizontal%20(59).png)

You’ve done it: You took an idea, built it into a thriving business, and now you’re ready to sell. Congratulations — few entrepreneurs make it to this point. You’re in the right place if you find yourself asking, “How do I sell my business?”

Now, it’s time to ensure you make the right deal for your most prized possession. Regardless of why you’re moving on, there are actionable steps you can take so that your business is sold at the right time, for the right price, and to the right buyer.

Table of Contents

- How to Sell a Business

- When to Sell Your Business

- How Much to Sell Your Business For

- Choosing a Path to Sell a Business

- Where to Sell Your Business

- Life After Exiting Your Business

How to Sell a Business

M&A is everywhere right now, according to Monique Swansen, Founder and CEO of Automated Accounting Services, a firm committed to supporting small and growing businesses. “Every group I’ve seen putting together conferences is talking about mergers and acquisitions as a tool for making an exit plan or growing your business,” she says.

Entrepreneurs choose to sell their businesses for many reasons, ranging from retirement and health problems to co-founder conflict and just plain boredom. In 2024, 9,456 small businesses were sold, a 5% jump from the year before.

With that in mind, here are the basic steps we recommend following

.webp)

Free Business Plan Template

The essential document for starting a business -- custom built for your needs.

- Outline your idea.

- Pitch to investors.

- Secure funding.

- Get to work!

Download Free

All fields are required.

Form not available

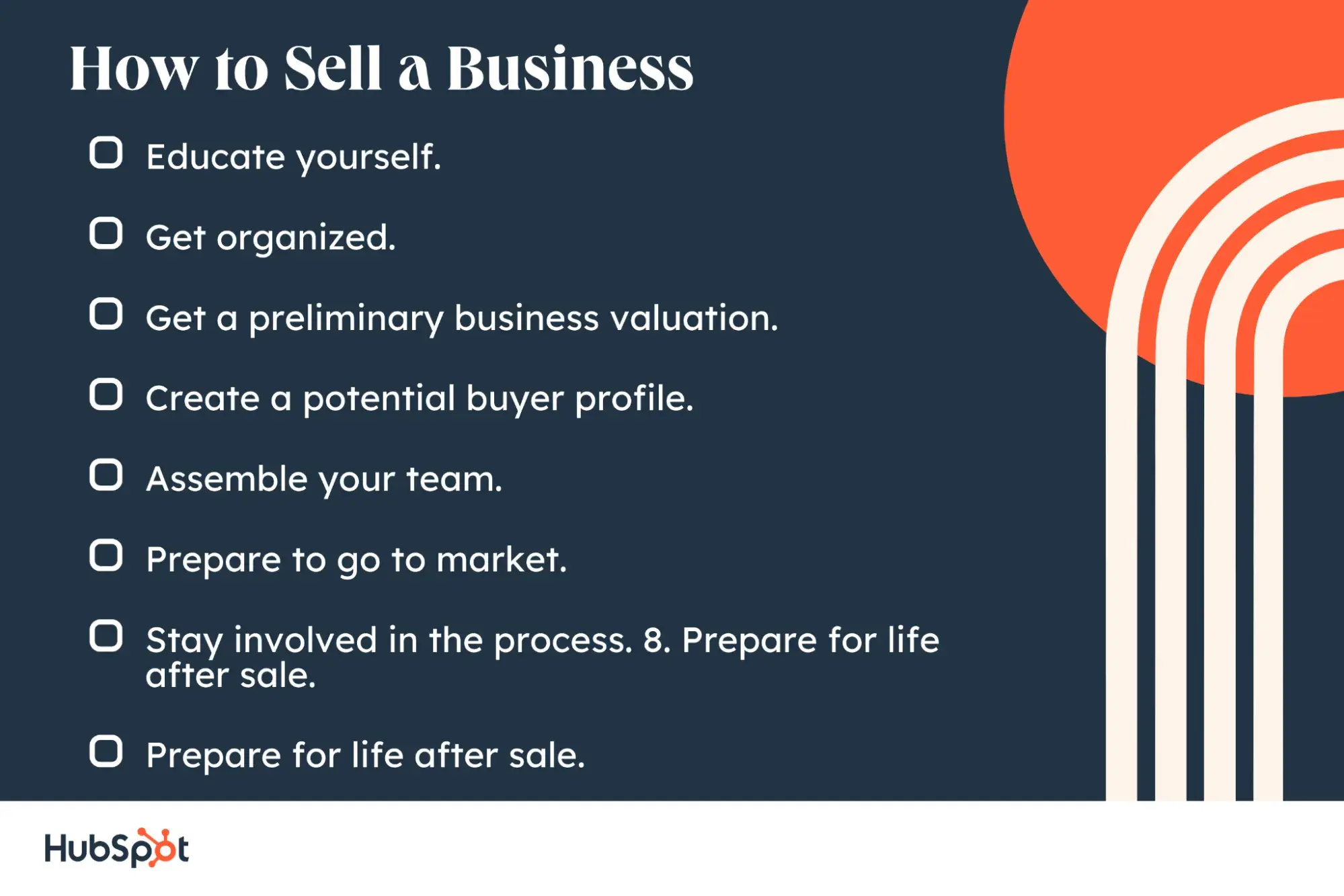

1. Educate yourself.

Spend some time researching how to sell (you’re doing that now!), and figure out if you need to make any changes to get your business ready for the process. Common actions include adding business processes to make the business scalable, adding features that would open up a new market, or filing patents to lock down intellectual property.

Tips to Get Started:

- Research recent business sales in your industry. You’ll want to understand market trends, pricing, and common deal structures.

- Identify areas where your business may need improvement. This might include streamlining operations, increasing profitability, or documenting workflows.

- Explore industry-specific resources. Consider M&A reports, exit planning webinars, and financial modeling tools.

2. Get organized.

Do your due diligence by gathering all of your documentation and getting ahead of anything that could slow down the sale (such as signoff from other shareholders or active lawsuits or legal proceedings). In addition to preventing delays, this step makes your business far more attractive to potential buyers. Here’s a breakdown of what you’ll need across the three main categories:

Financial Documents

It’s a good idea to create a financial packet with copies of important documents that can be shared with serious buyers during due diligence:

- Gather three to four years of financial statements, tax returns, and profit & loss reports.

- Outline all business assets, liabilities, and revenue streams to clearly identify what is included in the sale.

- Compile current lease agreements, outstanding loans, and supplier contracts to give buyers a full picture of ongoing obligations.

Legal Documents

It makes sense that your buyers will want to ensure the business is legally sound, so preparing legal documentation in advance can prevent last-minute delays:

- Verify ownership agreements, business licenses, and regulatory compliance records to confirm the business is properly registered and in good standing.

- Review employment contracts, NDAs, and any existing non-compete agreements to clarify obligations for both employees and buyers.

- Secure intellectual property rights, including patents, trademarks, and proprietary processes, to protect valuable business assets.

Operational Documents

- To ensure you get the top price for your business and plan for continuity after the sale, you’ll want to document your processes and operations:

- Develop a comprehensive operations manual detailing day-to-day processes and key workflows.

- Map out employee roles, leadership responsibilities, and key personnel contributions to ensure continuity after the sale.

- Evaluate physical assets, equipment, and business premises, addressing any necessary upgrades or repairs before listing.

- Implement systems and automation where possible to make the transition easier for new ownership.

Tips to Get Started:

- Tidy up your books. Verify that financials are accurate, debts are addressed, and records are clear.

- Assemble key documents. Organize essential agreements (leases, contracts, compliance records) in a structured format.

- Enhance operational efficiency. Fix inefficiencies, document processes, and ensure the business can function smoothly without you.

Free Business Plan Template

The essential document for starting a business -- custom built for your needs.

- Outline your idea.

- Pitch to investors.

- Secure funding.

- Get to work!

Download Free

All fields are required.

Form not available

3. Get a preliminary business valuation.

Turn to experts (e.g., business brokers, merger and acquisition advisers) to understand how much your company is worth, then consider if you’re willing to accept that price.

Tips to Get Started:

- Calculate EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). Your financial pros can help you do this and establish a financial benchmark.

- Research valuation for businesses in your industry. You’ll want at least a rough idea of what your business might be worth.

- Contact a business broker or valuation expert. Even if you’re not ready to hire them, getting their advice is a good starting point. An early assessment can also help you identify areas that could increase your potential sales price.

4. Create a potential buyer profile.

Find the why when thinking of your ideal fit. For example: Does the buyer have the cash to buy, or do they need financing? Have they bought companies before? Who would need to approve the deal on the buyer’s end (internally: founders, board members, management; externally: investors, banks)? Will they keep your team employed after the sale?

Tips to Get Started:

- Identify the type of buyer. Consider whether your ideal buyer is a strategic buyer (industry competitor, supplier, or partner) who wants to grow by acquisition or a financial buyer (private equity, individual investor).

- Think about financing vs cash. In addition to making or breaking the deal, it could affect the legacy you’re building if that’s important to you.

- Think beyond just the sale price. What do you want to happen to your employees, customers, and brand after the transition?

5. Assemble your team.

Putting together a team early can prevent a lot of stumbling down the road. Professionals who could help with the process include:

- Corporate finance attorney.

- Business broker.

- M&A adviser.

- Personal tax accountant.

- Company auditor.

- Sell-side bankers.

Tips to Get Started:

- Contact your existing experts. Do your current tax preparer, bookkeeper, or attorney offer these services? If not, can they recommend someone?

- Interview your options. Do they instill confidence and do you get along? You don’t have to be best friends but you do have to be able to trust them.

- Start early. Don’t wait until you’re 6 months out unless it’s an emergency. Instead, start this process several years ahead of time, even if you don’t end up selling, getting everything in order does you favors short term and in the long run.

6. Prepare to go to market.

For small businesses, owners can list their companies anonymously on business broker sites. For larger ventures, owners should identify potential suitors by looking at direct rivals and companies in related industries.

Tips to Get Started:

- Draft a confidential information memorandum (CIM) once selling is in your near future. This should contain details on financials, market position, and growth potential.

- Research small business sales platforms. BizBuySell, BizQuest, and Flippa are all examples where small business owners can discreetly list their companies for sale.

- Create a shortlist of potential buyers. Then explore outreach strategies through your industry network or a sell-side banker.

7. Stay involved in the process.

Deals can fall through days before closing; stay on top of it along the way by responding to requests within 24 hours, scheduling weekly calls with advisers, and pushing legal counsel to move documents forward quickly.

Pro tip: Time is your enemy. Resist any efforts made to push the closing date.

Tips to Get Started:

- Use a deal tracker. Doing so will help you stay on top of important deadlines, buyer requests, and negotiation points.

- Respond quickly to buyer-side requests. Getting organized ahead of time will make it easier to handle due diligence requests, legal paperwork, and buyer inquiries in an appropriate time frame.

- Be prepared for last-minute deal adjustments. You’ll need to work closely with your advisers to finalize the best possible agreement.

8. Prepare for life after sale.

Your business is your baby: You should be hands-on when planning your company’s transition (this includes how the new owner will interact with your employees and customers). But entrepreneurs also need to give thought to life after their exit, from retirement planning and managing sale proceeds to future personal and professional goals.

Tips to Get Started:

- Start thinking about your next steps. Do you want to launch a new venture, invest in other businesses, or take a break?

- Develop a tax-efficient plan for managing sale proceeds. Working with an advisor will make this easier.

- Decide on your role post-sale. Consider whether you’ll stay involved with your company in a consulting role or exit completely. If you’re staying involved, what are the conditions and terms?

When to Sell Your Business

Age is one of the reasons that Swansen is seeing such an uptick in small business owners getting ready to sell. “Lots of founders are getting closer to retirement age and are ready to pass the torch.”

She goes on to say that she also talks with lots of other business owners who started a company with the idea of selling, and now that things are flush, they’re ready to “make a profitable exit.

How do you know the right time to sell your business?

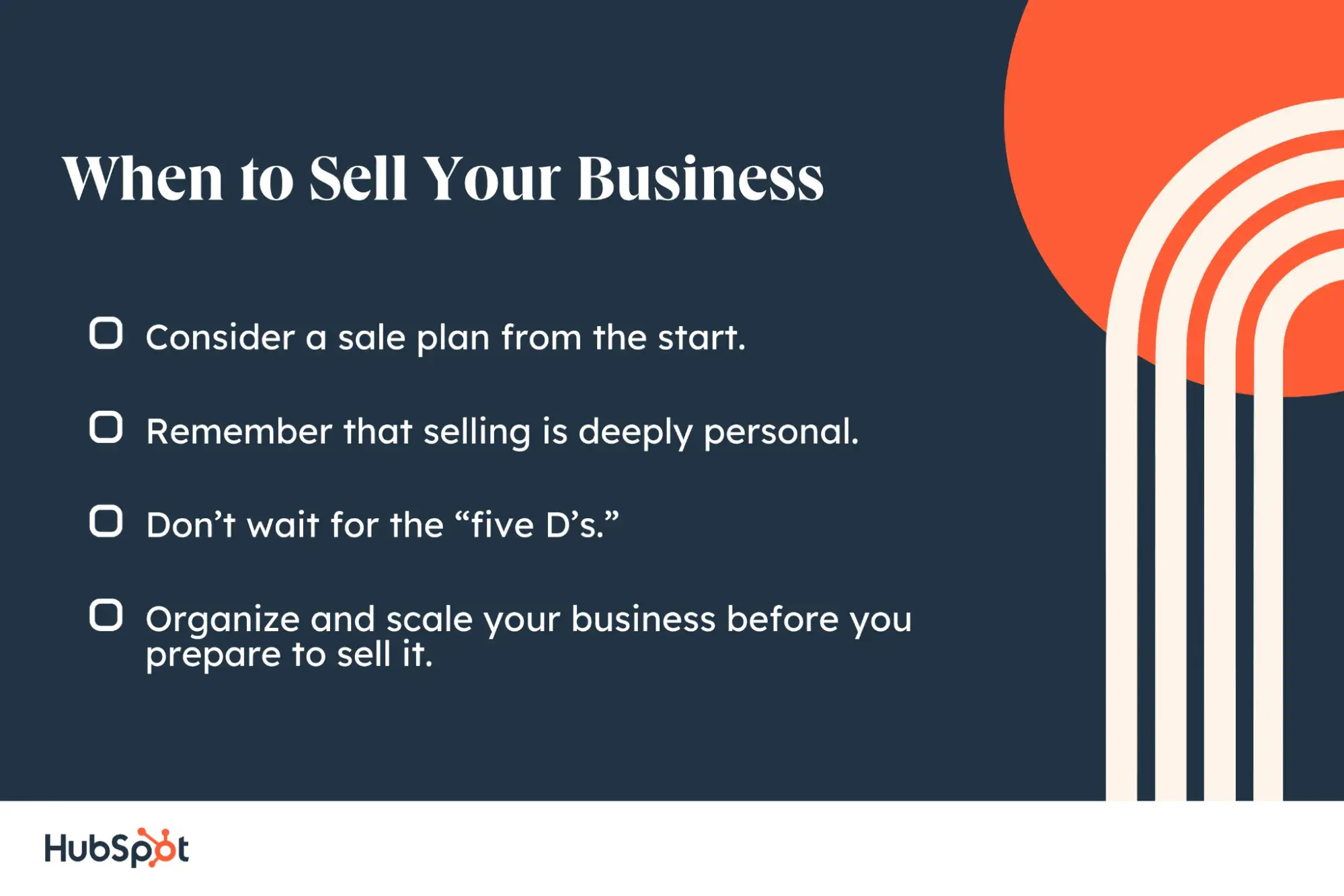

Knowing exactly when to let go of your venture can be intimidating, but one thing that most experts seem to agree on is that it’s best to decide early on if selling is in your future.

“The best time for entrepreneurs to consider selling their business is when they start their company,” says business broker Katie Milton Jordan. “Consider what you want your company to do for you. Are you creating a company that you want to sell or a company that will create an independent stream of income just for you?”

For those who start a business as a side hustle, that’s not always at the forefront, but choosing to sell your business isn’t something most companies can do on a whim.

When weighing the pros and cons of an exit, also think about the financial health of your company. “You want to be selling when your company is performing well, you’re cashed up, and you’re growing,” says David Raffa, a corporate finance expert. “The worst possible thing you can have is to sell in the slope part of your year.”

Selling your business is a deeply personal decision.

For Cindy Summers, founder of Sugar Fixé Pâtisserie, moving on felt right once her business no longer challenged her or fit her lifestyle.

“My passion is building businesses and creating great customer experiences. Once my business was established, I became more of an operator. This didn’t give me the mental gymnastics I needed to stay inspired,” she says.

Additionally, the nature of her business made it difficult for Summers to find work-life balance. “I was married but kid-free when I started the business. Three kids later and there was an emotional conflict between my family, employees, and customers. Busiest times in a bakery are weekends and holidays. This meant missing out on a lot at home,” she says.

Some other common life experiences that lead to exits include:

- Burnout.

- Illness

- Co-founder misalignment or conflict.

- Boredom.

- Retirement.

- Shifting life priorities.

Don’t wait for the “five D’s.”

Jordan advises owners to sell their companies before the “five D’s”: death, divorce, disease, disengagement, and downturn. Making an exit prior to those events can ensure you get a fair price for your creation.

“Most entrepreneurs tend to get out too late when they have no gas left in the tank, and the growth rate of the business is a big piece of the value you get in the end,” says Raleigh Williams, who sold his escape-room business for $26M. “Ending on a high note is something that pro exit entrepreneurs do versus amateurs.”

Free Business Plan Template

The essential document for starting a business -- custom built for your needs.

- Outline your idea.

- Pitch to investors.

- Secure funding.

- Get to work!

Download Free

All fields are required.

Form not available

Organize and scale your business before you prepare to sell it.

Swansen emphasizes the need to get your ducks in a row before you get anywhere close to the starting line of selling your business. As an accounting expert, she primarily focuses on the financial and operational aspects of preparing for a sale.

“If your business is well-organized, profitable, and growing at scale, with all of your financials ready to go, you’re probably going to get a higher purchase price,” she says.

So what does that look like?

Several years before you’re ready to exit, it’s a good idea to implement processes and get the right team members in the right places so you can create a turnkey operation.

That means using an integrated suite of tools to automate as much as possible — for example, HubSpot’s CRM and Marketing Hub are designed to work well together, which streamlines operations and makes it easier to create a positive customer experience.

As you get closer to going to market, it’s also important to get your financials in a row to paint the best possible picture for your potential buyers.

How Much to Sell Your Business For

Della Kirkman, a CPA and business investor, uses a simple calculation to get entrepreneurs started: “A quick and easy formula is to determine the five-year weighted average of EBITDA and multiply it by the range of multiples that are appropriate for your type of business.” Kirkman says she most often uses a multiple between three and five.

Get a professional valuation.

Meeting with experts to get a professional valuation of your business is the most accurate way to find the right number. Therefore, get started with assembling a team of advisers early in the selling process, and find professionals who work closely with your industry whenever possible. The more niche their experience, the more they’ll be able to guide your sale appropriately.

Third-party experts can also ensure the business is ready to be sold. “A lot of business owners don’t realize their company can’t be transacted and isn’t packaged properly to go to market,” Jordan says. “That’s why it’s important to ask questions and get educated as soon as possible.”

Step out of solopreneur mode and put on a CEO hat.

A common roadblock Jordan sees is solopreneur businesses. For those who wear every hat at their firm, buyers feel they are essentially buying a job rather than a company. Another reason for a difficult transaction could be if a business is tied up in any sort of legal proceedings.

Jordan suggests depersonalizing your operations to make a business more appealing to buyers.

“Business owners create a business and a system in a way that’s easy for them to run, built around their strengths and personality, because they work so hard around the clock,” says Jordan. “When it comes time to sell, their quirks are not the quirks of the new owner.”

She suggests that owners create manuals, standard operating procedures (SOPs), and automations where possible.

“Just like when someone buys a new car, and you hand them the set of keys and the owner’s manual,” she says. “If you have a company you can hand off with an owner’s manual, you have something that can be transacted.”

Once you have the right deal, stay active in the process until the very end.

“As a founder, so much of your net worth is tied up in this transaction,” Williams says. “Outsourcing that process and not being involved, or expecting a lawyer or broker to be as involved in the details to the same extent you need to be, is unwise.”

Choosing a Path to Sell a Business

As you can see, there are lots of considerations to make when selling your business. And because there are so many factors — including your industry, business size, and personal goals, among others — there’s no single best way to sell your company.

You’ll want to think about whether you want

- Total control over the process

- Someone to hold your hand every step of the way

- A quick exit

Depending on the complexity of your business and your level of M&A experience, it may feel like an obvious choice to go with a broker. There’s a reason that’s one of the most popular routes. However, many businesses choose to sell directly or go to auction as well. Each of the three comes with benefits and drawbacks, so I’m going to break them down below:

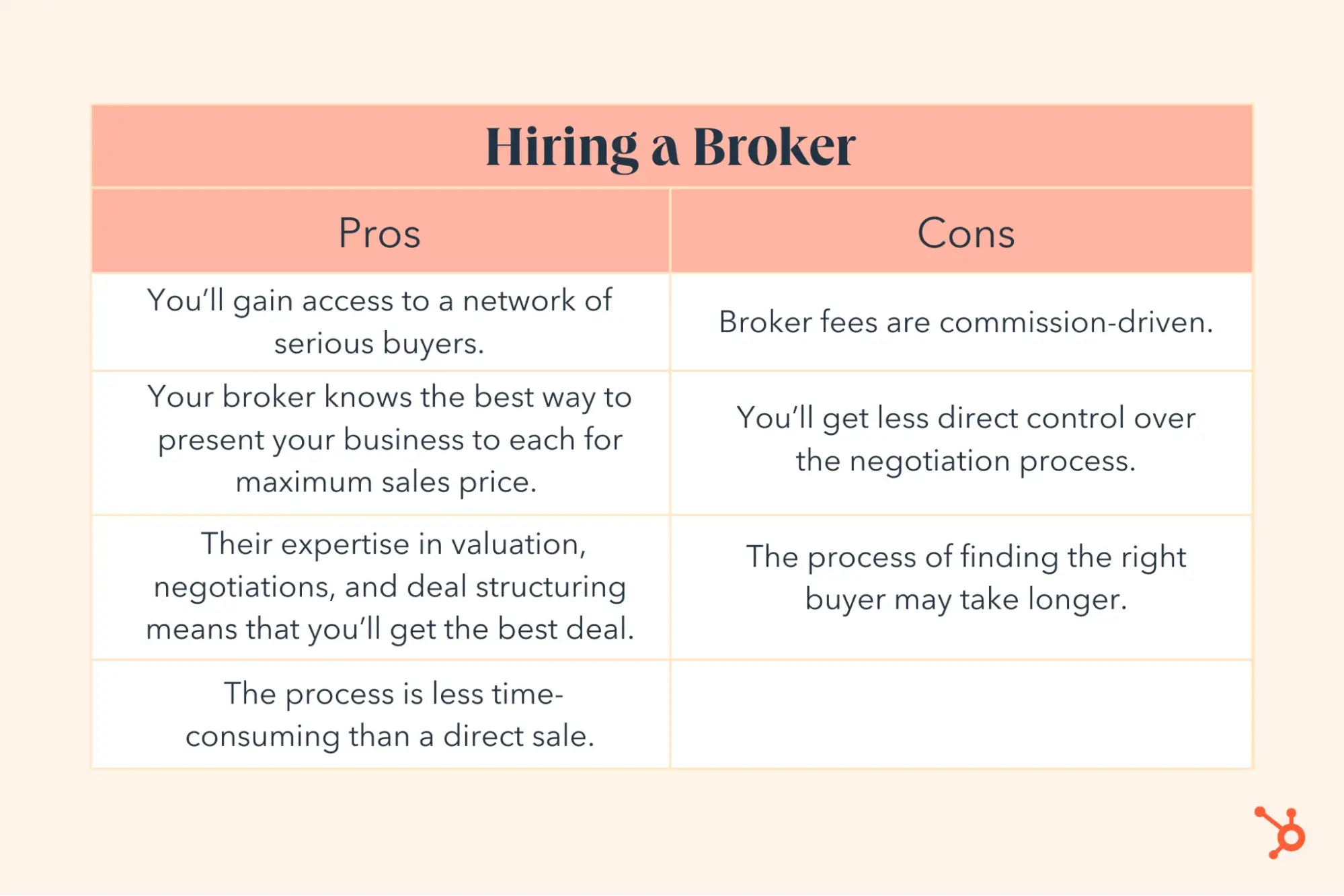

Hiring a Broker

A business broker or M&A adviser acts as an intermediary, connecting you with potential buyers and guiding negotiations. Brokers can help increase your sale price, handle complex paperwork, and streamline the process — but they come at a cost.

Pros:

- You’ll gain access to a network of serious buyers.

- Your broker knows the best way to present your business to each for maximum sales price.

- Their expertise in valuation, negotiations, and deal structuring means that you’ll get the best deal.

- The process is less time-consuming than a direct sale, which means you still have time to run your business.

- They manage the process for you and help you avoid common pitfalls.

Cons:

- Broker fees are commission-driven, meaning a significant portion of the sale price goes to them.

- You’ll get less direct control over the negotiation process.

- The process of finding the right buyer may take longer (then again, it may not if they have a turnkey buyer in their network).

Where to Start:

- Research brokers with experience in your industry and business size.

- Look for brokers accredited by organizations like the International Business Brokers Association (IBBA) or M&A Source.

- Discuss their commission structure, marketing strategy, and expected timeline before signing a contract.

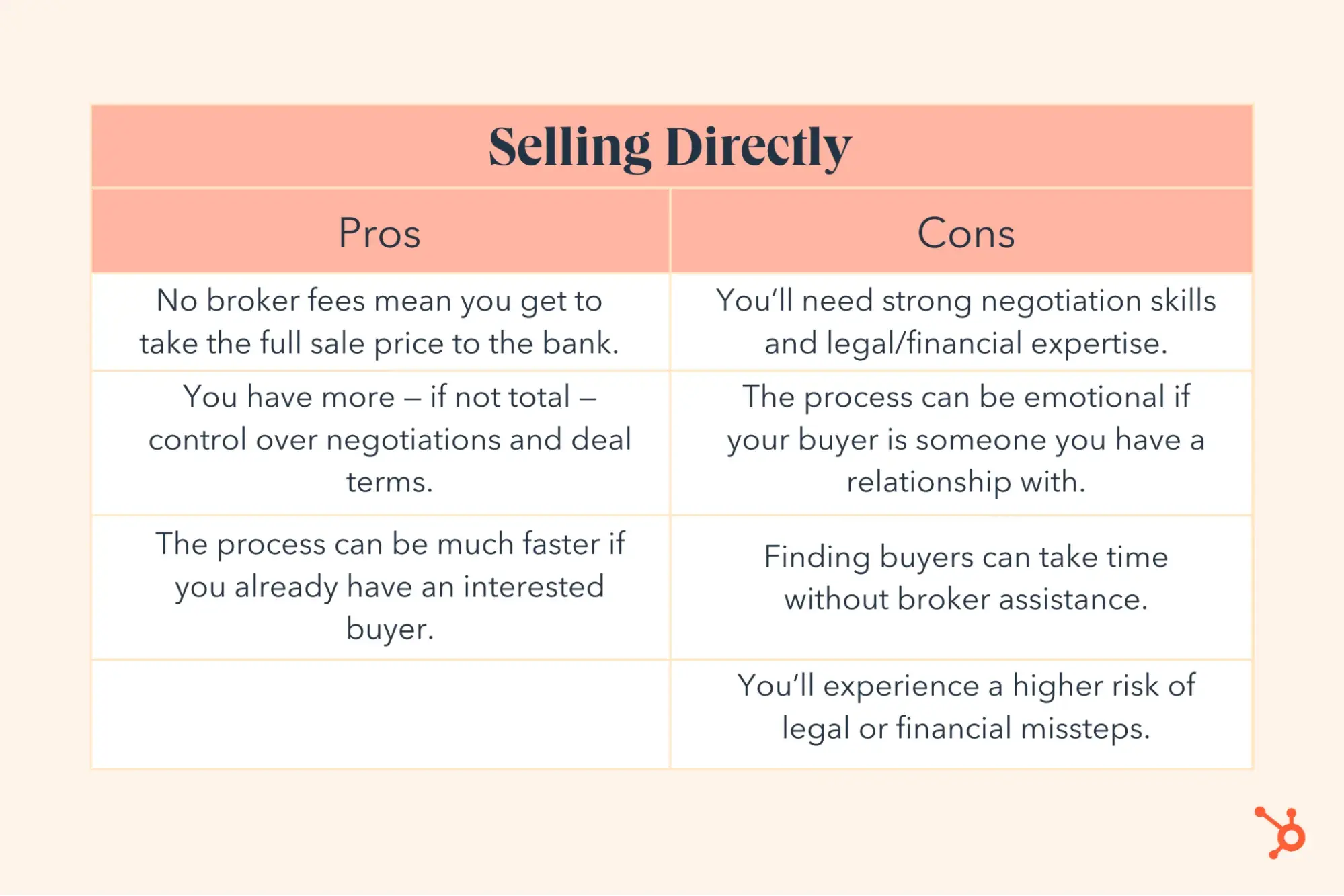

Selling Directly

Selling directly to a buyer gives you full control over the process. This is true regardless of who your buyer is, whether it’s a competitor, investor, employee, or even a family member. Experienced entrepreneurs who already have interested buyers and those who prefer to avoid brokerage fees often choose this option. However, there are trade-offs here as well.

Pros:

- No broker fees mean you get to take the full sale price to the bank.

- You have more — if not total — control over negotiations and deal terms.

- The process can be much faster if you already have an interested buyer.

Cons:

- You’ll need strong negotiation skills and legal/financial expertise.

- The process can be emotional and more personal if your buyer is someone you have a relationship with.

- Finding buyers can take time without broker assistance.

- You’ll experience a higher risk of legal or financial missteps.

Where to Start:

- Identify potential buyers from your industry, competitor list, or network. Keep in mind, they may be in a different region or neighborhood and want to grow by acquisition instead of scaling, so cast a wide net.

- Even if you’re not working with a broker, you’ll still want professional experts to support you, including an M&A attorney and financial adviser, to structure the deal properly.

- Consider listing your business on BizBuySell, BizQuest, or Flippa for additional exposure if you don’t have a buyer already lined up.

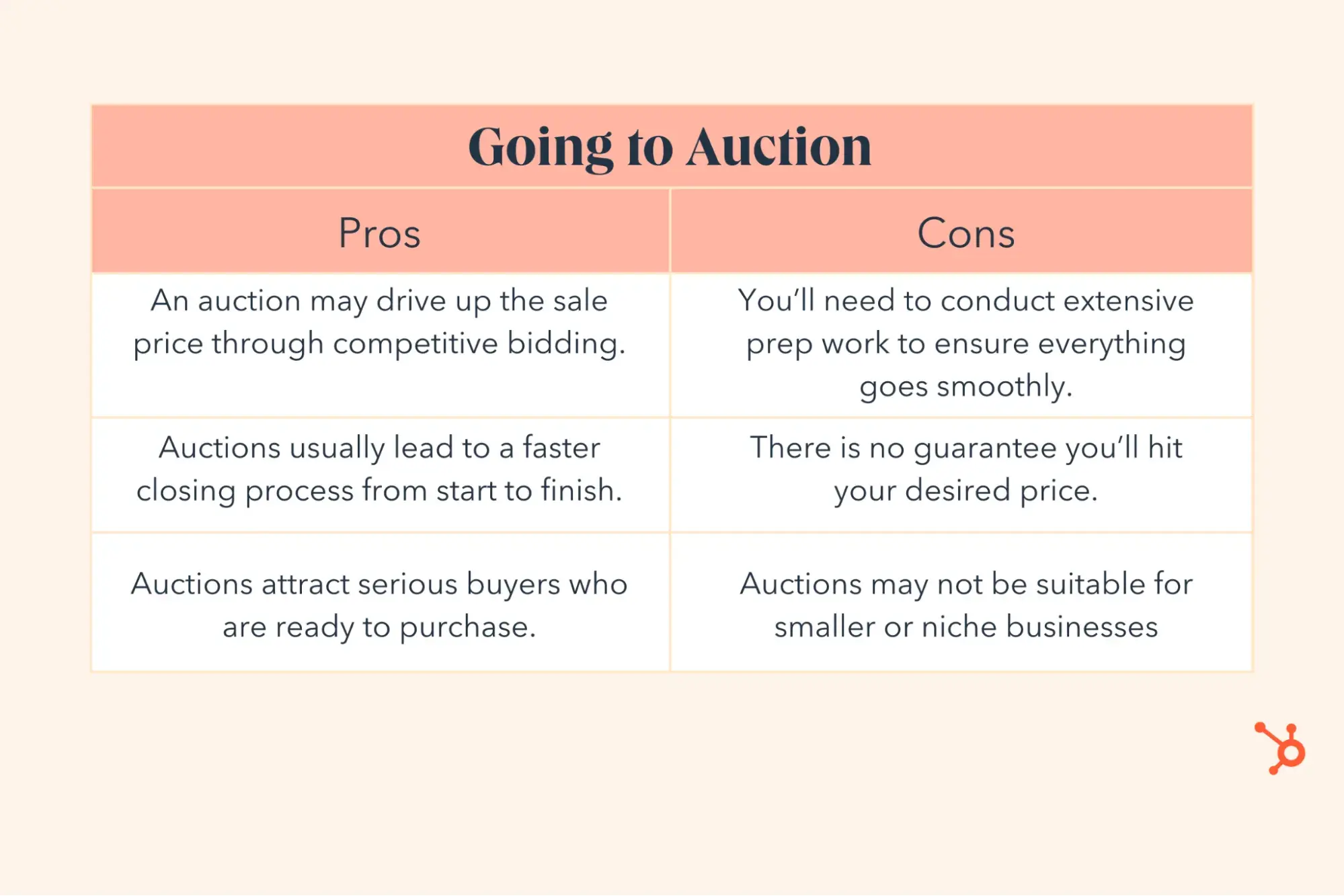

Going to Auction

If your business is in high demand or you need a quick sale, an auction process can be appealing. You might get multiple competing offers in a short period of time. However, keep in mind that auctions work best for businesses with strong financials, unique assets, or niche market positioning (though going too niche can also be problematic).

Pros:

- An auction may drive up the sale price through competitive bidding.

- Auctions usually lead to a faster closing process from start to finish.

- Auctions attract serious buyers who are ready to purchase.

Cons:

- You’ll need to conduct extensive prep work to ensure everything goes smoothly.

- There is no guarantee you’ll hit your desired price.

- Auctions may not be suitable for smaller or niche businesses.

Where to Start:

- Research auction platforms and decide whether you want an in-person or online auction.

- Much like the other sales processes, you’ll want to prepare all of your legal and financial documents well ahead of time. Your M&A advisor, attorney, and financial team can help here.

- Market the auction aggressively to attract high-quality bidders.

Where to Sell Your Business

If you’re wondering where to sell your business, the right place depends on its size. For small solopreneur-owned ventures, owners can list their companies anonymously on business broker sites such as BizBuySell).

There are many different business sites. Some target specific cities or states, as buyers often want to acquire local businesses. Experts recommend researching the best site to list using a simple Google search that includes your location.

Make a list of potential buyers.

For larger companies, Raffa says that entrepreneurs can spearhead the selling process directly through a sell-side banker rather than list on a business broker website.

“In that situation, you should do rounds of approaches,” he explains. “Make a list of 100 potential buyers, and start with the first 10-30 ideal ones, and work down that list.”

Raffa advises assembling your list by including companies 5-10x your size in your business space (often competitors), companies in a closely related space, companies in a similar industry who are struggling and need a new edge, and companies that want to enter your geographic market.

Create a plan for outreach.

He notes that when reaching out to potential buyers, likely only half will engage with you, and they should sign NDAs before you disclose further financial information and insider business details.

Alternatively, you can start with companies lower down the list to dip your toe in, understand the typical questions asked, and circle back to your ideal buyers when you feel more prepared.

When Williams began the process of finding a buyer, he approached direct competitors first, a tactic he says is helpful across industries.

“People in the same industry or adjacent to the industry are the easiest people to do deals with because they understand what they’re looking at,” he says.

It’s also common for business owners to get inquiries from companies or investors interested in acquiring. Even if a sale isn’t in your immediate plans, don’t ignore the opportunities, which may lay the groundwork for a deal down the road.

Free Business Plan Template

The essential document for starting a business -- custom built for your needs.

- Outline your idea.

- Pitch to investors.

- Secure funding.

- Get to work!

Download Free

All fields are required.

Form not available

Life After Exiting Your Business

Selling doesn’t have to mark the end of your career — your aspirations for the future can actually be baked into the terms of the sale.

“The options are endless,” says Kirkman. “Whatever they can dream up and negotiate into the deal, they can have.”

Kirkman says this includes options such as:

- Annuity in perpetuity: a profit share for the life of the business

- Retaining ownership of a brick-and-mortar building to create a future rent stream

- Taking a revenue share for any new clients brought into the company

- Selling your business on a partial installment basis to spread out the payments (which can help with tax deductions)

- Staying on as an employee (often called an acqua-hire)

- Stay with the business as a consultant

Whatever you choose, be sure to put time into the decision-making process. If a clean break feels like the right move, it likely is. If you’re not quite ready to say goodbye, that’s OK, too.

Plus, your exit might just be the first of many, and you can use the experience to inform your future ventures.

“Most entrepreneurs, after they’ve exited something, realize that the ends won’t justify the means nearly as much as they thought they would,” Williams says of running a business that’s purely profit-driven.

“They tend to actually move into the thing that they wanted to do all along but were scared there wasn’t enough money in,” says Williams. “And they tend to make way more money in the thing they actually enjoy doing than their first exit.”

Free Business Plan Template

The essential document for starting a business -- custom built for your needs.

- Outline your idea.

- Pitch to investors.

- Secure funding.

- Get to work!

Download Free

All fields are required.

Form not available

Business Growth

![How Entrepreneurs Navigated (& Survived) Recessions [New Data & Expert Tips for Economic Slumps]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/Copy%20of%20Featured%20Image%20Template%20Backgrounds%20(55).png)

![What Is a Joint Venture? [+ How It Can Grow Your Business]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/joint-venture-1-20250423-541905.webp)

![Grants for Black-Owned Businesses and Other Funding Resources for Black Business Owners [+ Deadlines for 2025]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/copy%20of%20jade%20walters%20btb%20(41).png)

%20(1)-1.png)

![How Startups Are Raising Money Today [Data + Expert Insights]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/Copy%20of%20Featured%20Image%20Template%20Backgrounds%20(62).png)

![Here's How to Value a Company [With Examples]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/Value%20a%20Business%20fi%20(1).png)