.png?width=112&height=112&name=Image%20Hackathon%20%E2%80%93%20Horizontal%20(59).png)

%20(1)-1.png)

After (a lot of) research, I realized that small business insurance isn’t a one-size-fits-all expense. Costs vary based on factors like industry, coverage type, and risk level. If you’re currently searching for insurance, understanding common price ranges can help you navigate quotes and find the best policy for your needs.

Table of Contents

- What is small business insurance?

- How much does small business insurance cost?

- Examples of Small Business Insurance Costs

- Small Business Insurance Costs by State

- Small Business Insurance Costs by Industry

- How is the cost of small business insurance calculated?

What is small business insurance?

Small business insurance can include multiple types of policies that protect a business’s employees, assets, income, and intellectual property. Commercial property insurance, business income insurance, and general liability insurance are some examples that fall under the general umbrella of small business insurance.

Many insurance companies will offer combined coverage, which I find is important for multifaceted businesses. You might need to protect your assets, employees, customers, and income. One of the most common combined policy options includes a business owner’s policy (BOP), which usually includes property and liability coverage.

.webp)

Free Business Plan Template

The essential document for starting a business -- custom built for your needs.

- Outline your idea.

- Pitch to investors.

- Secure funding.

- Get to work!

Download Free

All fields are required.

Importance of Small Business Insurance

I’ve learned one thing about running a business — accidents don’t ask for permission. And when they happen, I don’t want to be scrambling to cover costs or, worse, dealing with a lawsuit that could have been avoided with the right insurance.

If one of my employees gets injured on the job or a customer slips in my store, I’m responsible. Without workers’ comp or general liability insurance, I’d be paying those medical bills out of pocket. Alarmingly, 75% of small businesses are underinsured, leaving many owners vulnerable to such incidents.

And it’s not just about physical injuries. I’ve seen businesses grab images off the internet for their signage, thinking it’s no big deal — until they’re slapped with a copyright lawsuit for using something they didn’t have permission for. Yet, only 17% of small businesses have cyber insurance, exposing them to digital risks.

Then there are the big disasters. Think: break-ins, fires, natural disasters. If something happens to my storefront, I want to know I have the coverage to rebuild without draining my bank account.

Pro tip: Create a solid business plan to not just stay on track but also to secure the right insurance. If you need a starting point, grab HubSpot’s free Business Plan Template to lay out your mission, customers, finances, and risk strategy. Insurers love a business with a clear plan, and so will you.

Get Your Free Business Plan Templates Today

How much does small business insurance cost?

Your small business insurance coverage depends on factors like industry, location, number of employees, and the specific types of coverage needed. A sole proprietor working from home won’t have the same insurance needs as a retail store with employees and foot traffic.

Pro tip: Before buying a policy, I always recommend assessing potential risks. If you handle customer data, cyber liability insurance might be crucial. If you own a storefront, general liability is a must.

Average Cost for Small Business Insurance

On average, small business insurance costs between $500 to $1,500 per year (or about $42 to $125 per month). But remember, these numbers can shift based on how much coverage you choose.

Here’s an example: If I opt for a business owner’s policy (BOP) at around $57 per month, then add general liability coverage for $42 per month, my total monthly cost would be about $99.

Pro tip: Bundle your policies. Many insurers offer discounts if you purchase multiple policies together, like a BOP combined with cyber liability. I bundled mine and cut my costs by 15%.

Free Business Plan Template

The essential document for starting a business -- custom built for your needs.

- Outline your idea.

- Pitch to investors.

- Secure funding.

- Get to work!

Download Free

All fields are required.

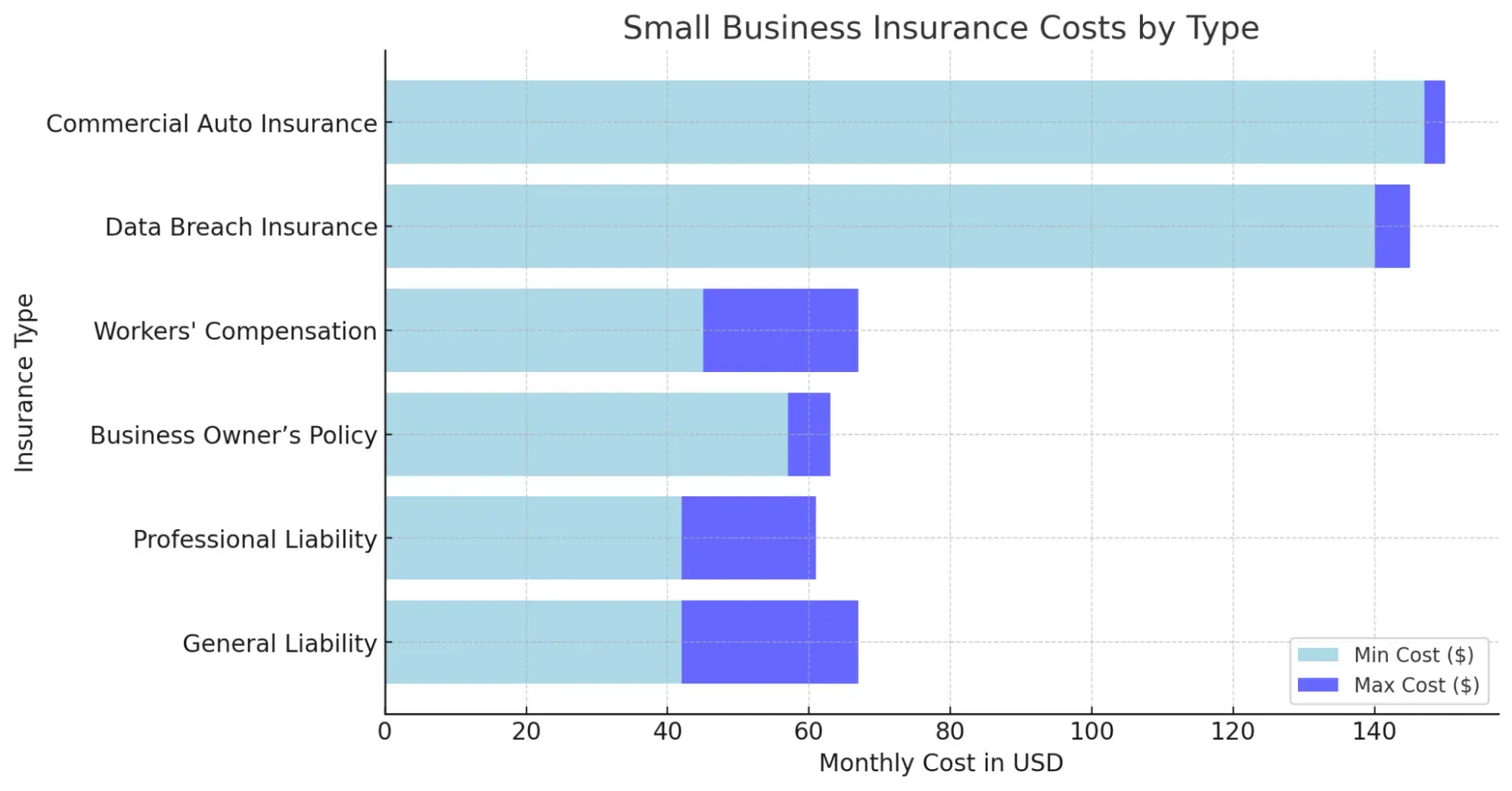

Small Business Insurance Costs by Type

Different types of insurance provide different protections, and the price varies accordingly. Some policies cover income loss or intellectual property, while others protect physical assets or provide coverage for injuries.

Here are some common categories of small business insurance:

- General liability. Covers property damage, bodily injury, defamation, or libel and costs around $42–$67 per month. I’ve seen businesses hit with unexpected lawsuits that cost $54,000 on average, according to The Hartford. This coverage can be a lifesaver if someone sues over an accident at your business.

- Professional liability (errors & omissions insurance). Protects against claims of mistakes or negligence and costs about $42 to $61 a month. If I were a consultant or service provider, this would be a no-brainer. Even a small oversight could lead to a legal battle, and this policy helps cover legal fees and settlements.

- Business owner’s policy (BOP). Combines general liability and property insurance and costs typically $57 to $63 per month. I like this option because it’s a bundled package, making it easier (and often cheaper) to get essential coverage in one go.

- Workers’ compensation. Covers medical expenses and lost wages for work-related injuries and costs about $45 to $67 per month (varies by state). Most states legally require this if you have employees. Skipping it isn’t worth the risk — penalties can be $10,000 or more in some places.

- Data breach (cyber liability) insurance. Covers costs related to cyberattacks and data breaches and costs about $140 and $145 a month. With 61% of cyberattacks targeting small businesses, I wouldn’t take chances. A breach can cost businesses $120,000 to $1.24M, which is enough to put many out of business.

- Commercial auto insurance. Covers company-owned vehicles and costs between $147 and $150 per month (varies by location). If my business had delivery vans or company cars, I’d need this. Personal auto insurance won’t cover business-related accidents, and the cost of an uninsured accident could be devastating.

Examples of Small Business Insurance Costs

Business insurance is important. Take workers’ compensation, for example. I might pay around $50 a month, or $600 a year. That might sound like a lot until I consider that the average workers’ compensation claim costs around $42,000. That’s not a risk I’m willing to take. If I owned a restaurant, I’d be even more cautious — burns alone can cost tens of thousands of dollars per claim.

Then there’s commercial auto insurance. If my employees drive for work, I need coverage. Motor vehicle accidents are one of the top workplace injuries, with costs going over $90,000 per incident. I can’t afford to take that kind of financial hit, so I’d rather have insurance covering me when the unexpected happens.

It’s also tempting to think, “Data breaches won’t happen to me,” but hackers don’t discriminate. If my tech stack went down due to a cyberattack, I could be locked out of my systems until I paid thousands in ransom. Worse, if customer data were stolen, I’d be looking at $140-$160 per record compromised. If hundreds or thousands of records get leaked, I’m looking at a six- or seven-figure disaster.

I don’t take chances with my business, and neither should you.

Small Business Insurance Costs by State

Where I run my business plays a big role in how much I’ll pay for insurance. If I’m in a highly populated area or somewhere prone to natural disasters, I can expect my premiums to be higher than if I were in a more rural location with fewer risks like flooding, hurricanes, or wildfires.

Here’s a look at average small business liability insurance costs based on location:

- California: $55 per month

- Colorado: $53 per month

- Florida: $58 per month

- Georgia: $69 per month

- Illinois: $46 per month

- New York: $65 per month

- Oregon: $48 per month

- Pennsylvania: $60 per month

- Texas: $59 per month

- Virginia: $35 per month

Free Business Plan Template

The essential document for starting a business -- custom built for your needs.

- Outline your idea.

- Pitch to investors.

- Secure funding.

- Get to work!

Download Free

All fields are required.

Small Business Insurance Costs by Industry

What I do for a living affects my insurance costs. If I run a high-risk business — like a construction company or a brick-and-mortar store — I’ll pay more than someone working solo from home, like a freelance writer.

Here are some average monthly premiums for a BOP in different industries:

- Cosmetics and salons: $550 per month

- Pharmacy: $700 per month

- Retail: $800 per month

- Real estate: $600 per month

- Construction and landscaping: $900 per month

- Marketing: $300 per month

- Freelance writer: $130 per month

- Restaurant: $1,000 per month

Pro tip: I made the mistake of almost jumping on the first quote I found — until I compared multiple providers and found a better deal. Shopping around can save you hundreds.

How is the cost of small business insurance calculated?

When I first looked into the average insurance cost for small businesses, I was surprised by how many factors influenced small business insurance costs. Here’s a quick rundown:

1. Industry and business type.

High-risk industries like construction or manufacturing tend to have higher premiums because of the potential for injuries or property damage. On the other hand, lower-risk businesses like consulting or marketing usually pay less. Since every industry has different risk levels, insurers adjust rates accordingly.

2. Business location.

If you operate in an area prone to natural disasters, high crime rates, or strict local regulations, expect to pay more for coverage. For example, a business in a flood zone or a city with a high rate of theft will have higher property insurance costs compared to one in a safer location.

3. Business size and revenue.

If you have more employees, a larger physical space, or high revenue, your exposure to liability increases — which means insurers will charge more. A business with just a few employees and a small office will generally pay less than a large company with multiple locations.

4. Coverage types and policy limits.

If you want extensive coverage with high limits, you’ll have a higher premium. But if you’re willing to accept a higher deductible (meaning you pay more out-of-pocket before insurance kicks in), you can reduce your premium. The key here is balancing coverage and affordability.

5. Claims history.

If you’ve had previous insurance claims, you might have to pay more for coverage. Insurers see frequent claims as a sign of high risk. So, keep a clean claims record — it shows you have a well-managed business that’s not prone to constant issues.

6. Risk management measures.

One of the smartest things you can do to keep your insurance costs down is to invest in risk management. Think: Installing security systems, training employees on workplace safety, and following best practices. It makes the business less risky in the eyes of insurers. Some companies may even offer discounts if you take proactive steps to minimize risks.

Pro tip: Adjust coverage as your small business grows. Your insurance needs will evolve as your business expands. I review my policies annually to make sure I’m not overpaying or underinsured.

Protect your business with small business insurance.

I never fully grasped how one unexpected event could financially wreck a business until I saw the numbers. I always knew insurance mattered, but when I really looked into it, the reality hit hard. One accident, one lawsuit, one disaster — any of these could mean tens of thousands in losses, if not more. In some cases, it could be enough to shut everything down for good.

What really changed my perspective was realizing that business insurance isn’t just another line item on my expenses — it’s a safety net for everything I’ve built. It covers damages and protects my employees, customers, property, and income. No matter what industry I’m in, the right coverage is a must.

Free Business Plan Template

The essential document for starting a business -- custom built for your needs.

- Outline your idea.

- Pitch to investors.

- Secure funding.

- Get to work!

Download Free

All fields are required.

Business Growth

![How Entrepreneurs Navigated (& Survived) Recessions [New Data & Expert Tips for Economic Slumps]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/Copy%20of%20Featured%20Image%20Template%20Backgrounds%20(55).png)

![Grants for Black-Owned Businesses and Other Funding Resources for Black Business Owners [+ Deadlines for 2025]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/copy%20of%20jade%20walters%20btb%20(41).png)

![Here's How to Value a Company [With Examples]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/Value%20a%20Business%20fi%20(1).png)