.png?width=112&height=112&name=Image%20Hackathon%20%E2%80%93%20Horizontal%20(59).png)

The good news is your business doesn’t have to be another casualty. In this post, I’ll walk you through the five stages of entrepreneurship and the common pitfalls you should avoid in each. You’ll also see real-life examples of entrepreneurs at each stage.

Table of Contents

- What are the five stages of entrepreneurship?

- The Process of Entrepreneurship

- The Five Stages of Entrepreneurship

- Dream Big

The Process of Entrepreneurship

Entrepreneurship is the process of turning innovative ideas into a business. It involves identifying opportunities, developing solutions, and creating value.

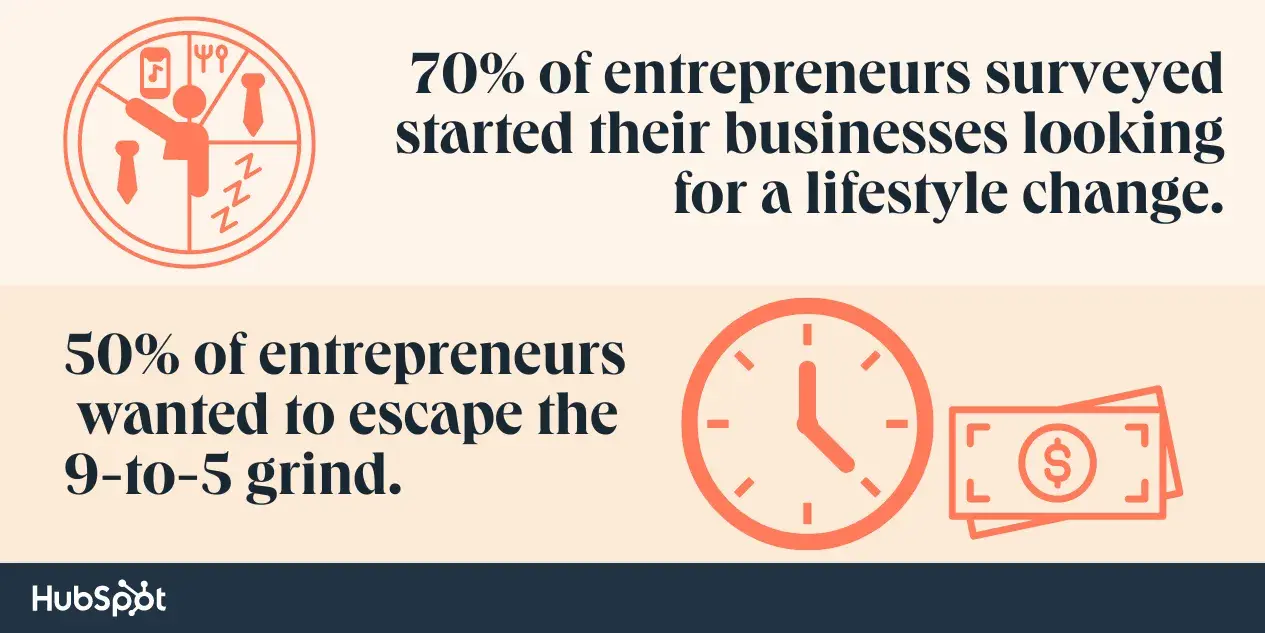

I've noticed that while some entrepreneurs (26% to be exact), like myself, follow a passion (in my case, writing), many others start their ventures seeking a career change. In fact, HubSpot research found that about 70% of entrepreneurs surveyed started their businesses looking for a lifestyle change. Nearly half wanted to escape the 9-to-5 grind — which is something I can definitely relate to!

The first step for entrepreneurs is to identify a business opportunity, driven by innovation, a market need, or a personal passion. They then brainstorm and refine their ideas and conduct market research to validate their concepts. As the vision takes shape, entrepreneurs develop business plans, secure funding, and assemble teams to bring their ideas to life.

This process is part of the broader entrepreneurship cycle, which encompasses all stages — from ideation to eventual exit or sustained growth.

One thing I‘ve learned is that successful entrepreneurs constantly iterate their products or services based on customer feedback. I’ve seen this firsthand with my own writing services — as I'm always adapting my offerings based on client needs and market demands.

Entrepreneurship Trends Report

Unlock the future of entrepreneurship with this free report from HubSpot and The Hustle.

- 92% of entrepreneurs have no regrets about starting their business.

- 61% find customers through powerful word-of-mouth referrals.

- 37% of entrepreneurs are targeting higher ARR in the next year.

- And more trends!

Download Free

All fields are required.

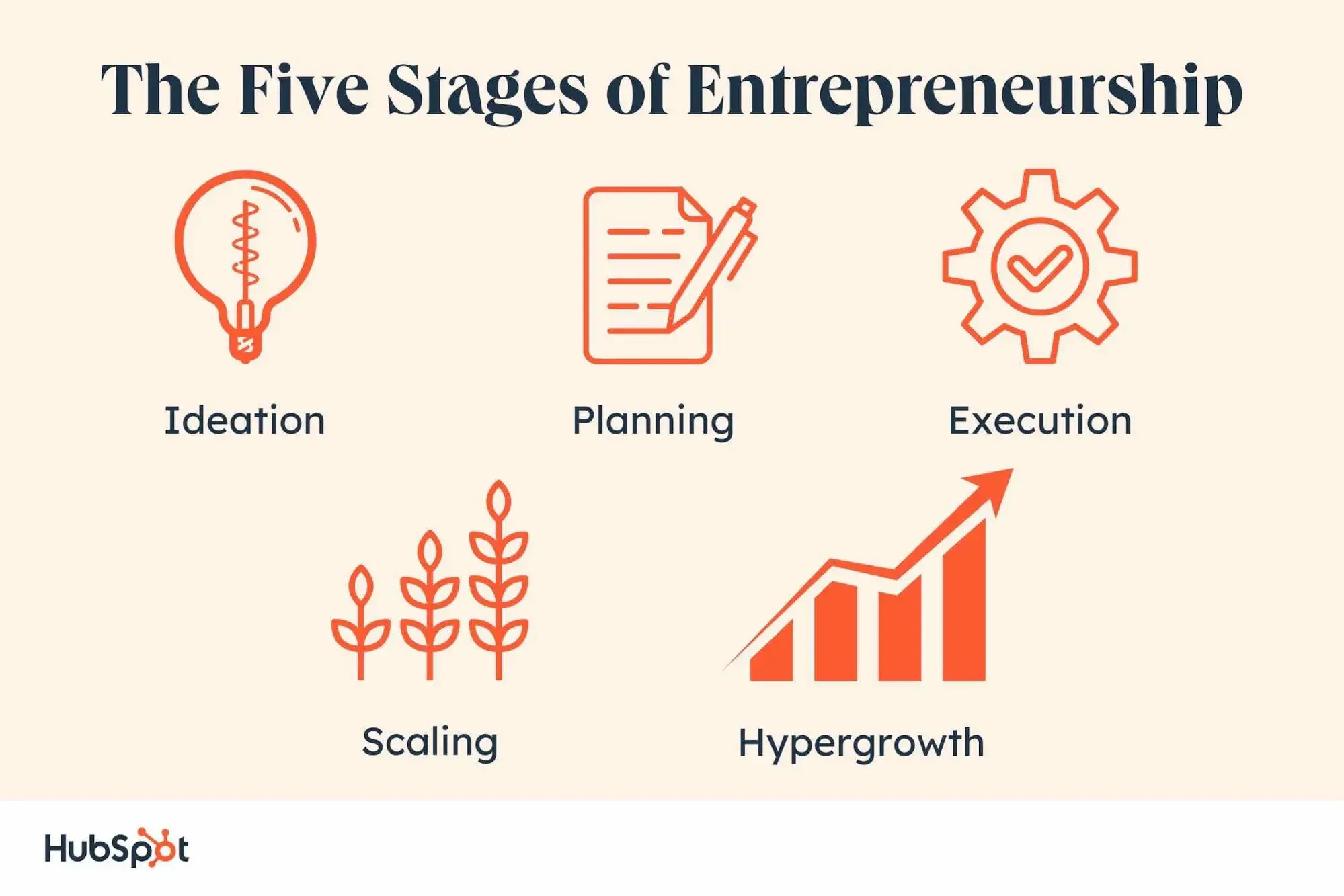

What are the five stages of entrepreneurship?

The “Five Stages of Entrepreneurship” is a simple framework that helps new founders to understand the entrepreneurship journey. The stages include ideation, planning, execution, scaling, and hypergrowth.

The Five Stages of Entrepreneurship

In my journey as a freelance writer and through my work with various startups, I've experienced each of the five distinct stages of entrepreneurship. I find this framework incredibly helpful for understanding the entrepreneurial journey, both for myself and for the founders I work with.

Let me walk you through each stage.

Stage 1: Ideation

Ideation is where it all begins. I remember when I first decided to become a freelance writer – I was filled with ideas and possibilities. The goal at this stage is to identify and validate a profitable business idea.

Here are three common ways entrepreneurs develop ideas:

- Considering what they’re passionate about. For a role model, turn to Nike Co-founder Phil Knight. His interest in shoes and sports strongly influenced his decision to start the athletic shoe company.

- Identifying a problem in an existing market. This is how the idea for Uber came about. Travis Kalanick and Garrett Camp were returning from a LeWeb, an annual tech conference. It was a cold winter night, and unfortunately, they couldn’t get a cab. So they asked themselves, “What if you could request a ride from your phone?” The rest is history.

- Focusing on niche markets. A niche market is a small, underserved segment of a large and established market. Jacamo, for instance, is a clothing retail company targeting larger (and taller) men who typically struggle to find large-sized, fashionable clothes.

- Observing and addressing community needs. Some entrepreneurs find inspiration by immersing themselves in their community and identifying unmet needs. As Armen Gazaryan, the founder of CalltheCare, a non-emergency medical transportation service, explains: “Be in your community, live it true, and recognize real problems that exist. Real problems need genuine solutions by truly understanding the pains of your target audience.”

After an initial brainstorming session, you’ll need to narrow your scope and focus on one idea. I’ll explain how you can validate concepts below.

Idea Validation

Ensuring the viability of your idea is essential. When you confirm the market need for your product, you avoid the risk of pouring your resources into a business idea that’s a dud.

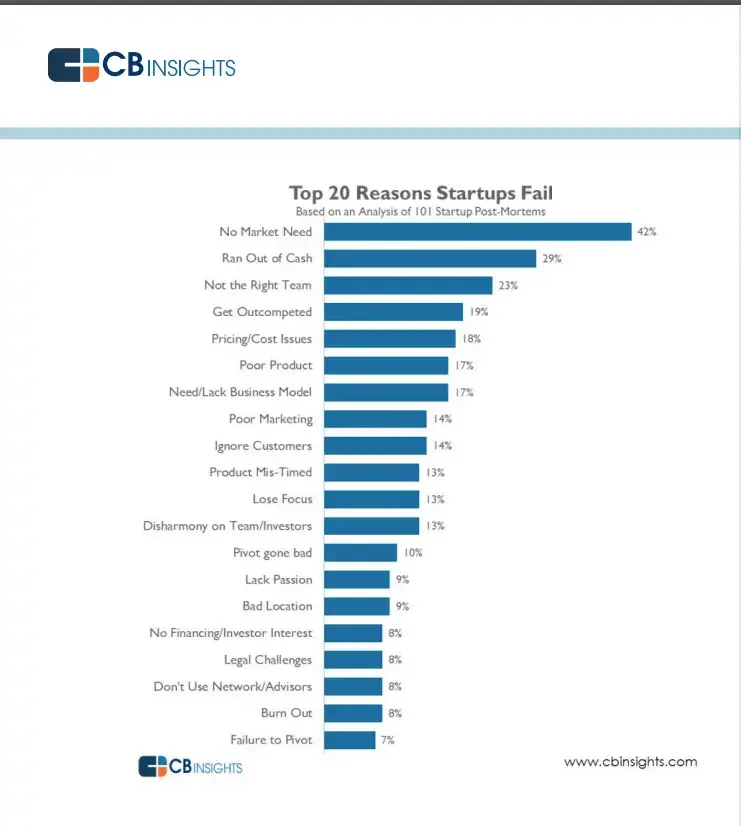

Most entrepreneurs skip this crucial step. They assume there’s a market for their product without validating their hypothesis. The result? They build a product that no one wants, causing their businesses to die in infancy.

A CB Insights Report reveals this is one major reason businesses fail. Don’t make the same mistake.

If you’re unsure of a market’s potential for your idea, think twice before committing resources to it.

How to Validate Your Business Idea

One way to validate your idea is to evaluate the performance of similar businesses. A perfect example is Chanty.

Chanty is a communication and team collaboration app that went head-to-head with companies like Slack. When Chanty came on the scene, Slack was already dominating the market and raking in millions of dollars in revenue. This proved to Dmytro Okunyev, Chanty’s Founder, that they could get a slice of the market.

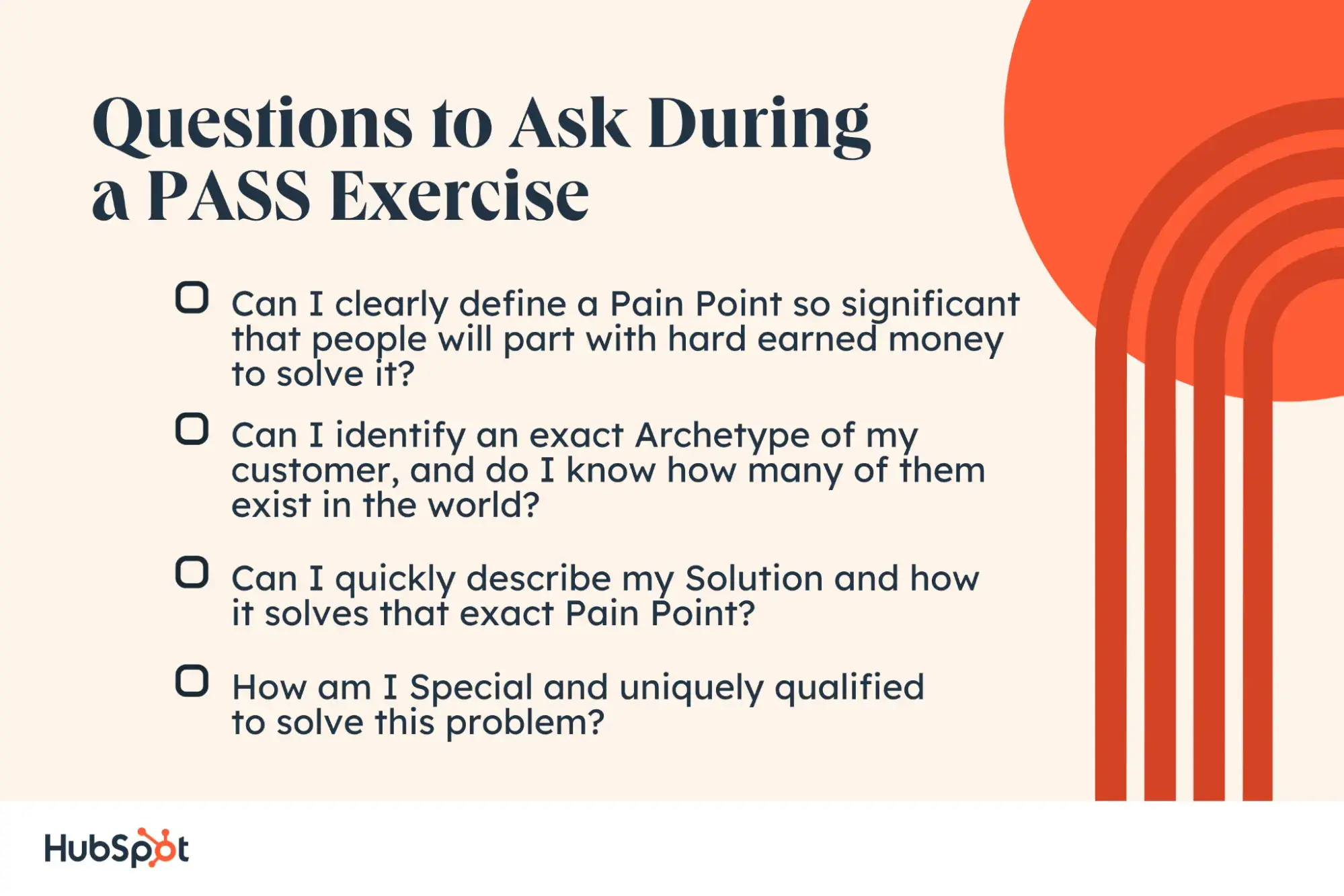

Another SMART approach is to use a structured framework to assess your idea's viability. Heather Lawver, Founder and CEO of Ceemo.ai, a brand and pitch deck creation tool, shares a powerful method she calls “Take a PASS At It”:

"When I'm first developing an idea for a company, I like to Take a PASS at it! That stands for Pain Point, Archetype, Solution, and Special: four simple questions that lay the foundation for your business plan and your future marketing narratives,” Lawver says.

According to Lawver, questions include the following.

“If you can clearly answer all of those questions, you'll be on your way to a solid business plan and a compelling marketing narrative,” Lawver says.

To show it in practice, Lawver shares she answered those questions for her startup, Ceemo.ai.

- Pain Point: Data-backed, strategic marketing is far too expensive for early stage startups, leaving founders with empty aesthetics that limits their growth.

- Archetype: There are 472 million entrepreneurs in the world, one-third of whom are first-timers who likely aren’t familiar with how to craft strategic marketing.

- Solution: Ceemo generates brands based on Crunchbase market data & seamlessly applies your new brand across all the marketing & pitch assets you need.

- Special: I have a uniquely holistic skill set that I’ve used to help founders raise over $170 million in venture capital.

Lawver's framework provides a systematic way to validate your idea and identify its market potential.

You can also validate your ideas during discussions with trusted peers. As David Darmanin, founder of Hotjar, says, “Step one of validating an idea is reaching out to your personal networks and gauge response. This differs from approaching friends and family who will always want to be nice to you.”

Another handy way is to contact your network via email, social media, and many online communities. Done right, you can get free and unbiased advice that’ll help you iterate on your business idea quickly.

The lean start-up methodology also provides a comprehensive approach to testing business ideas. To learn more about the lean start-up, read this book by entrepreneur Eric Ries.

Stage 2: Planning

In my experience, planning is where many great ideas fall apart. Just as architects need building plans, entrepreneurs need business plans.

I always advise my clients to develop a solid plan, but I also remind them of a quote from one of my favorite entrepreneurs, Mark Zuckerberg: “Ideas don't come out fully formed. They only become clearer as you work on them. You just have to get started.”

When I started my freelance writing business, my plan was pretty basic. But over time, as I worked with more clients and gained more experience, my vision became clearer and my plans more detailed.

Tools like HubSpot's Business Plan Templates can be incredibly helpful in this process and provide a structured framework for developing a comprehensive business plan.

Here’s a preview of the marketing plan page from one of the templates:

Developing a business plan helps you estimate costs, identify risks, and set up risk mitigation measures. A written business plan is even more essential if you’re seeking investors in your company. Potential investors want to see the extent to which you envisioned your business.

For this reason, put lots of thought into your plan, create a document that’s thorough, and consider your long-term goals.

Note that you don’t need to write a 37-page business plan or have a 15-year forecast before you begin building your business. As Mark Zuckerberg said, “Ideas don’t come out fully formed. They only become clearer as you work on them. You just have to get started.”

So, if you don’t have a five-year vision of your business yet, don’t let that stop you from taking the first few steps while you flesh out the big picture.

Stage 3: Execution

Like a plane stuck on a runway, many budding entrepreneurs often generate some momentum, but they never lift off. As a result, many innovative ideas never become a reality.

I remember when I landed my first client. I was terrified!

What if I couldn‘t deliver what they wanted? What if they didn’t like my work? But I pushed through that fear and executed my plan. That first project led to more, and soon, I had a thriving business.

The fact is, ideas are a dime a dozen, but execution is rare. To succeed, you’ll need to become adept at putting a plan into action.

This is where tools like HubSpot's Starter Bundle Built for Startups and Small Businesses can be invaluable. You get a suite of tools to help you manage customer relationships, marketing, and sales as you launch your business.

This stage is crucial, as 38% of entrepreneurs find achieving their first $100K in Annual Recurring Revenue (ARR) to be the hardest milestone.

Starting a business is risky and scary. And that feeling of uncertainty — the fear of failure and of making mistakes is one of the major reasons entrepreneurs hesitate to execute.

If you’ve identified and planned out your big idea, you’re probably filled with the excitement of “what could be” and the fear of “what if it doesn’t work?” simultaneously.

You’re not alone. Founders like Dmytro Okunyev had these mixed emotions, too.

Today, Chanty is thriving because Dmytro mustered the courage to move forward with his plans despite the uncertainties.

So, recognize that your plan isn’t foolproof. You will make mistakes. But just as you can’t paddle a boat tied to the dock, you can’t steer your business toward your vision until you launch and tackle your mistakes head-on.

Moving too slow or too fast is dangerous. So caution is necessary either way. Develop a good sense of when to act fast, get rid of your desire for perfection, and know when to slow down.

The bottom line: business is trial and error. Make peace with the fact that you’ll make mistakes. Take small calculated bets. Learn from the resulting failures and move forward.

If you believe in your idea, you’ve tested it, the timing feels right, and you have assembled your team, then launch!

Entrepreneurship Trends Report

Unlock the future of entrepreneurship with this free report from HubSpot and The Hustle.

- 92% of entrepreneurs have no regrets about starting their business.

- 61% find customers through powerful word-of-mouth referrals.

- 37% of entrepreneurs are targeting higher ARR in the next year.

- And more trends!

Download Free

All fields are required.

Stage 4: Scaling

Scaling is all about growth, and it comes with its own set of challenges. In my freelance writing business, scaling meant taking on more clients and higher-paying projects. For many of my clients, it involves expanding their customer base, improving their products, or entering new markets.

So you face an important question: “Should you bring in external investors and give up equity or bootstrap your business, i.e., self-fund through personal savings, debt, or customer funding?”

Founders of successful companies often bootstrap in their early days, but eventually, they accept outside investment. However, outliers like Spanx bootstrapped their way to a unicorn valuation after founder Sara Blakely started the undergarment company using only $5,000 of her personal savings.

Here are some pros and cons of bootstrapping:

Pros:

- Full control of your business

- Forces you to find smart growth strategies

- No pressure from external investors

Cons:

- Relies on sweat equity

- Can be more stressful

- Slower growth potential

On the flip side, accelerated growth is one major benefit that investor-backed start-ups enjoy. GitHub, an internet hosting service for software development, is an example of a business that scaled fast thanks to external funding.

Tom Preston-Werner, Chris Wanstrath, and PJ Hyett founded GitHub in 2008 and funded it for four years. In 2012, they got their first VC investment of $100 million and raised another $250 million in 2015. By October 2018, their annual recurring revenue was between $200-$300 million. Microsoft bought GitHub for $7.5 billion in the same year.

Whether you bootstrap or get investor backing, three factors are crucial for scaling your business quickly:

- Building effective systems. A system is a structure that fuels the smooth running of your business without your presence or supervision. These systems clearly outline how your company operates.

- Learning to lead. Learn to sell a vision to your team. You must be able to inspire others to act. This way, you leverage other people’s talents and experience to achieve results. Alone, you can only go so far.

- Track your profitability. It’s not unheard of to find a business with $50 million in revenue but $200k in profit. That’s why you shouldn’t focus on growing sales alone. Instead, obsessively track your margins and brainstorm ways to increase them.

Implementing robust Sales Software like HubSpot’s can help you manage your growing customer base and track your sales metrics as you scale.

When scaling, it‘s also easy to get caught up in immediate growth concerns. However, I’ve learned that it's crucial to think about the long-term trajectory of your business. This includes considering potential exit strategies, even if they seem far off.

Logan Rae, Founder at Argon Agency, shared an insight that resonated with me:

"When I started my first company, I was so focused on the early stages that I couldn‘t imagine needing an exit strategy. But, I quickly learned that planning your exit is a huge part of the scaling process. It helps you make calculated decisions and align your growth with potential future outcomes, whether that’s selling to a larger brand or going public.

“I‘ve found this advice invaluable. Imagining different exit scenarios has helped me make more strategic decisions in my own business, even though I’m not planning to sell anytime soon.”

Hiring While Scaling

As you scale, hiring also becomes a critical consideration. Traditional full-time hires aren‘t always the best solution, especially when you need specialized skills but can’t justify a full-time salary.

I've found great success with fractional hiring, a strategy echoed by Jennifer Cresswell, Founder and Principal at consulting firm Thoughtgro:

"When scaling my PR agency, we needed highly experienced professionals but couldn't afford them full-time. We turned to fractional talent — hiring contractors for specific engagements. This allowed us to provide top-tier service without overextending financially."

I‘ve applied this approach in my own business, bringing in editors for specific projects. It’s allowed me to take on a wider range of clients and deliver high-quality work without the overhead of full-time employees.

To learn more about how to build systems, read:

- The E-Myth Revisited: Why Most Small Businesses Don't Work and What to Do About It

- Built to Sell: Creating a Business That Can Thrive Without You

Stage 5: Hypergrowth

Hypergrowth is a season of rapid and exponential growth that companies experience as they scale. Specifically, an organization experiences hypergrowth when its Compound Annual Growth Rate (CAGR) exceeds 40% and remains so for at least a year, according to the World Economic Forum.

For context, “normal growth” companies have a CAGR of 20%. “Rapid growth” companies have a CAGR of 20% to 40%. Some companies that have achieved hypergrowth include Amazon, Slack, Stripe, Zoom, Uber, and Bolt.

While not all businesses reach this stage, 37% of entrepreneurs anticipate higher sales or ARR in the coming year, showing optimism for growth.

Hypergrowth is characterized by rapid, exponential growth. I‘ve had the privilege of working with a few companies in this stage, and it’s both exhilarating and challenging.

Achieving hypergrowth is desirable but challenging. One common setback is the risk of employee burnout from overwork. A prolonged period of unprofitability is another prevalent challenge.

This pattern of pursuing hypergrowth at the expense of short-term profitability is the norm with high-growth businesses.

To enter this phase of exponential growth, focus on the following three factors.

1. Product Innovation

Hypergrowth is demand-driven. So unless you build a product that customers love, you’ll never get there. Harsh, but true.

Customer-centricity is an obsession for (all) hypergrowth businesses, not just a “core value” they hang on the walls. They constantly leverage empathy, data, and customer feedback to build the best products.

2. Agile and Scalable Systems

What got you to $10 million in ARR won’t get you to $900 million. The systems that run small businesses efficiently will not support your hypergrowth.

Uber had to overhaul its driver onboarding process multiple times to support its hypergrowth. Until 2013, drivers had to go to a local office to complete some paperwork in order to become an employee. Then, they morphed into an online application process that allowed drivers to sign up without visiting a local office.

And when they began international expansion, the company had to design another process to accommodate the differences in regulations across host countries.

3. A Core Team

Hypergrowth is driven by hyper-effort. That’s why long work hours are common in hypergrowth companies. It’s a hard grind. And if you don’t have a team that shares your passion and believes in your mission, you’re not going far.

Whatever you do, don’t try to achieve hypergrowth too fast. Companies attempting to scale prematurely often push their operational capabilities to the limit, increase their stress levels, and hurt their business reputation.

To learn more about hypergrowth, read:

Dream Big

Throughout my journey as an entrepreneur and working with various startups, I‘ve learned that success isn’t just about having a great idea — it's about execution, perseverance, and adaptability.

My biggest takeaway is that the entrepreneurial path is rarely linear. I‘ve seen firsthand how important it is to test ideas, iterate quickly, and build a strong support network. I’ve also realized that setbacks are inevitable, but they're often the best teachers. The entrepreneurship cycle has taught me to embrace challenges as opportunities for growth.

As I continue on this path, I‘m reminded of Steve Jobs’ words: “The people who are crazy enough to think they can change the world are the ones who do.” This mindset keeps me motivated, even when faced with doubters or obstacles.

Entrepreneurship Trends Report

Unlock the future of entrepreneurship with this free report from HubSpot and The Hustle.

- 92% of entrepreneurs have no regrets about starting their business.

- 61% find customers through powerful word-of-mouth referrals.

- 37% of entrepreneurs are targeting higher ARR in the next year.

- And more trends!

Download Free

All fields are required.

Entrepreneurship

![Inside Holding Companies — The Entities That Own Popular Businesses [+ Expert Tips]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/holding-companies-1-20250502-5640825.webp)

![Grants for Black women and women of color [+ 2025 deadlines]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/grants-for-black-women-1-20250328-4679344-1.webp)

![Everything You Need to Know about Partnership Businesses [+ Expert Tips]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/partnership-business-1-20250219-4868724.webp)

![Entrepreneurial Marketing: Find New Customers on a Shoestring Budget [+Expert Tips]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/entrepreneurial-marketing-1-20250220-651487.webp)

![Entrepreneurship Trends That Will Change the Business of Building Businesses in 2025 [Expert & Data-Backed Predictions]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/entrepreneurship-trends-1-20250219-7312699.webp)