.png?width=112&height=112&name=Image%20Hackathon%20%E2%80%93%20Horizontal%20(59).png)

Table of Contents

- What is a business legal structure?

- Four Types of Business Structures

- Think Bigger Than Your Current Situation

What is a business legal structure?

A business legal structure, or business entity, is a classification of a company and how it operates. It also regulates your federal and state tax obligations.

There are four primary categories:

- Sole proprietorship.

- Partnership.

- Limited liability company (LLC).

- Corporation.

When I first started, I carefully considered whether I‘d want to bring on partners or scale my business later. I’ve discovered how expensive and time-consuming it can be to change your business structure down the road, so I always advise thinking about your future plans when choosing a business structure.

.webp)

Free Business Plan Template

The essential document for starting a business -- custom built for your needs.

- Outline your idea.

- Pitch to investors.

- Secure funding.

- Get to work!

Download Free

All fields are required.

Form not available

Four Types of Business Structures

|

Feature |

Sole Proprietorship |

LLC |

Partnership |

Corporation |

|

Formation Costs |

$0-100 |

$100-800 |

$200-1,000 |

$500-2,000 |

|

Liability Protection |

None |

Full |

Varies by type |

Full |

|

Tax Treatment |

Personal tax only |

Pass-through |

Pass-through |

Double taxation (C-Corp) |

|

Paperwork |

Minimal |

Moderate |

Moderate |

Extensive |

|

Raising Capital |

Difficult |

Moderate |

Moderate |

Easiest |

|

Management |

Owner only |

Flexible |

Shared |

Board of Directors |

|

Example Clients |

Freelance writers |

Small agencies |

Marketing firms |

HubSpot, enterprises |

|

Growth Potential |

Limited |

Good |

Moderate |

Highest |

|

Asset Protection |

None |

Strong |

Varies |

Strongest |

|

Common Use Case |

Starting out |

Growing consultancy |

Shared expertise |

Enterprise SaaS |

|

Personal Tax Impact |

Direct |

Pass-through |

Pass-through |

Salary + Dividends |

|

Exit Strategy |

Simple closure |

Can be sold/transfer |

Complex dissolution |

Stock sale/merger |

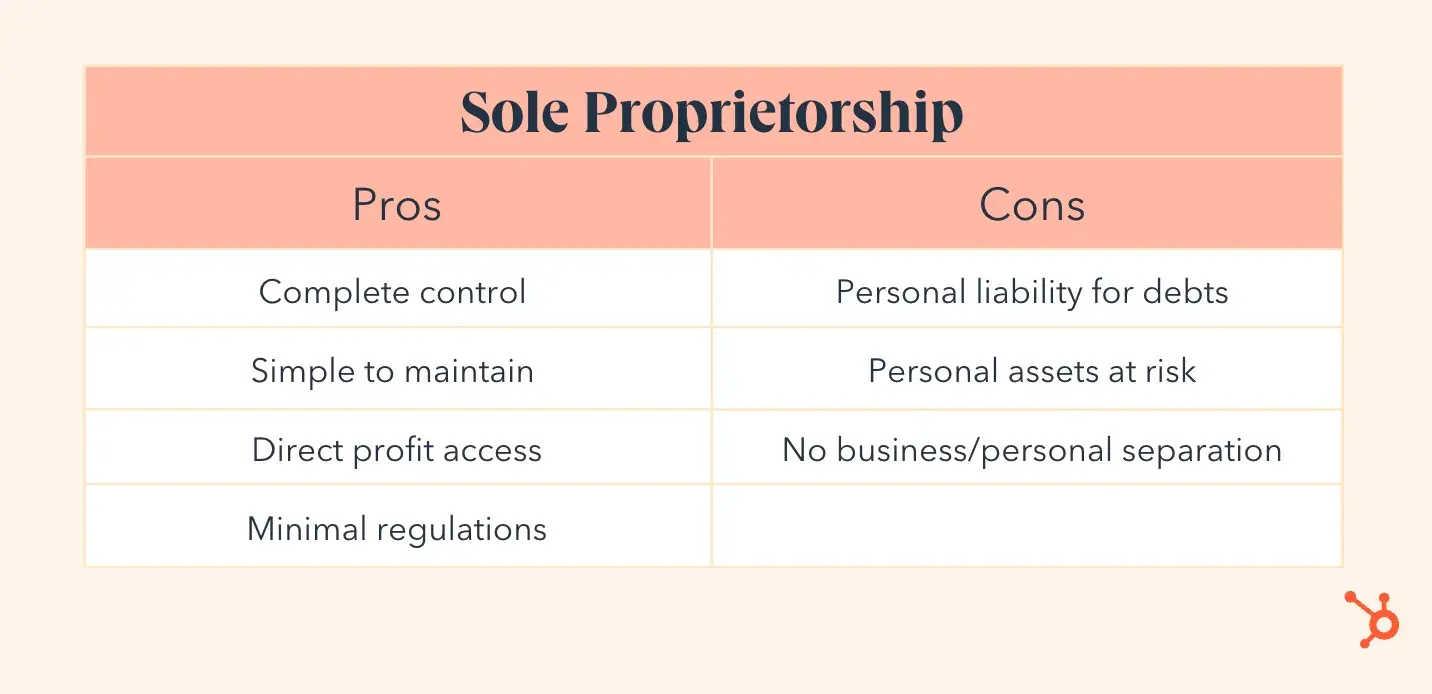

1. Sole Proprietorship

A sole proprietorship is the easiest business structure to start. In fact, when I first began freelancing, I discovered there‘s no setup involved — you’re automatically considered a sole proprietor.

This means you own and operate the business as one individual — there’s no difference between the owner and the business. You file taxes under your legal name or the name of the business you registered with the Division of Corporations.

Here’s a snapshot of the pros and cons of sole proprietorships.

The only way around this is to purchase business insurance and include liability waivers in contracts. Another option is to transfer or share personal assets with someone else.

For taxes, sole proprietors must pay federal and state income taxes, depending on where they operate. Some states don’t charge income taxes for sole proprietorships, such as Florida.

It’s free to establish a sole proprietorship, but if you register a Doing Business As (DBA) name, you’ll pay between $10 and $100.

Examples of sole proprietors include freelancers, gig workers, and small business owners like writers, web developers, hair stylists, and online store owners.

Example: Content Writing Services

I started my B2B SaaS content consulting business as a sole proprietorship, which was the simplest way to begin. I wrote blog posts, whitepapers, and case studies for software companies under my own name, filing taxes with Schedule C.

While this structure worked initially, I realized that as I took on larger enterprise clients and higher-value projects, I needed more liability protection and growth potential.

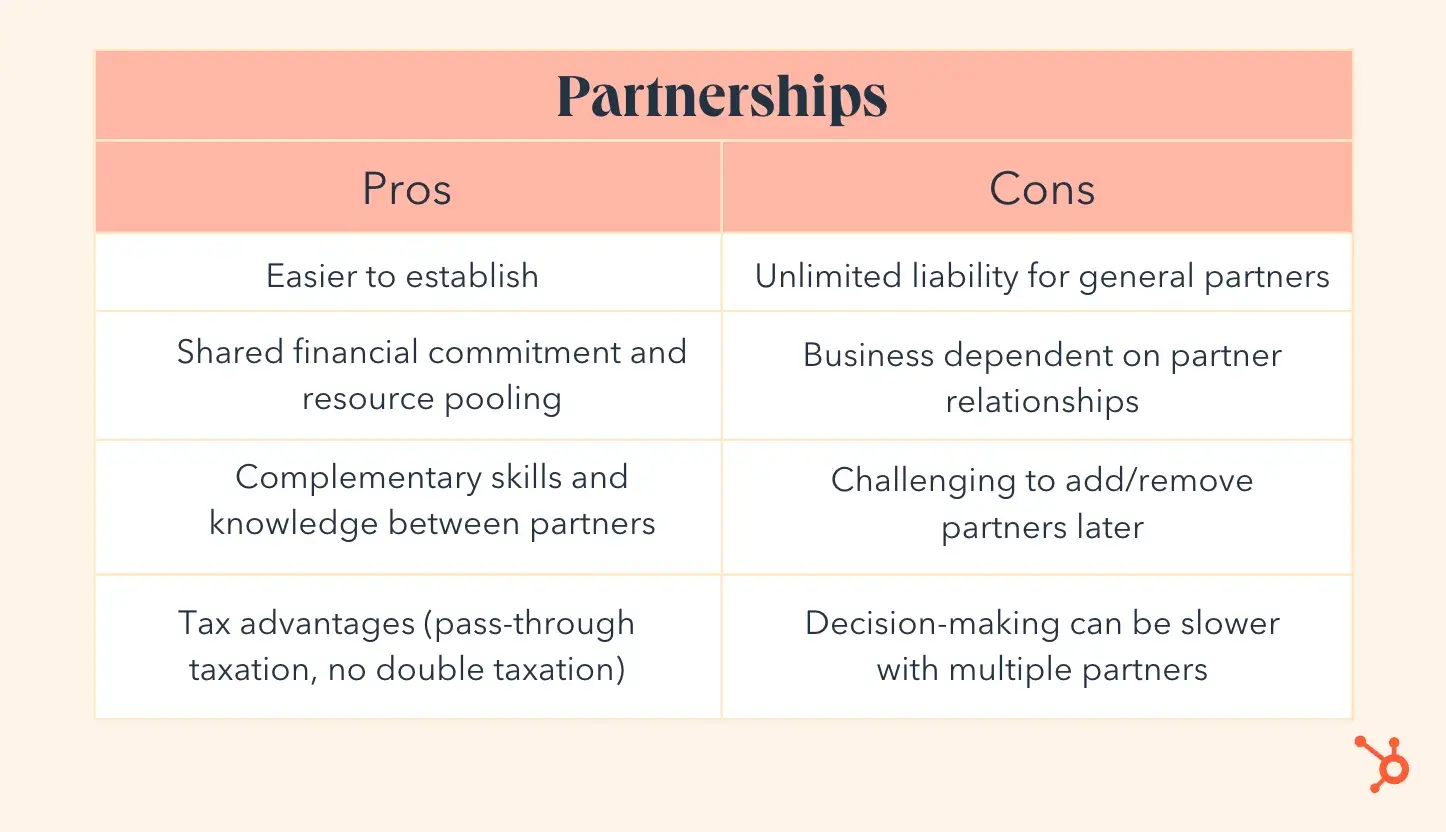

2. Partnership

A partnership is like a sole proprietorship, except two or more people own it. There are two types of business partnerships:

- Limited liability partnerships (LLP).

- Limited partnerships (LP).

In an LLP legal business structure, each partner has limited liability. The partners’ personal assets are off-limits in litigation and for debt repayment. Plus, partners are protected from the actions of other partners.

So if one co-owner gets sued for misconduct, the other partners aren’t responsible for the costs that incur.

An LP is a little different — one or more general partners (GPs) have unlimited liability, and the other owners have limited liability. Some differences include:

|

LPs |

GPs |

|

Only liable for debt up to the amount they’ve invested |

Part owners have specialized knowledge and skills in the industry, so they take part in business operations (e.g., doctors or lawyers in a practice) |

|

Can make business decisions as long as it’s in line with what’s in the partnership contract |

Personal assets are susceptible to seizure to repay business debts (there’s no limit to how much the GP can be liable to repay) |

|

Has authority to act on the company’s behalf, without permission or knowledge of the LPs |

All partners decide the voting power LPs will have, which can be restricted to certain areas. For example, an LP may have 20% voting power because they invested 20% of the capital in the company and can only vote on matters revolving around equipment purchases and acquisitions.

The partnership agreement details the roles and rights of each partner to prevent future conflicts and is critical to have before establishing the business.

It should outline:

|

Profit and loss sharing |

What percentage each partner receive in profits and losses — equal or based on the contributions/investments of each partner |

|

Dissolution terms |

What happens if one or more partners decide to leave the business voluntarily or involuntarily (e.g., death, incapacitation, breach of agreement, etc.) |

|

Management rights and responsibilities |

What each owner will control in the business and their duties (e.g., finances, operations, etc.) |

|

Capital contributions |

How much each owner will invest in the company to launch and maintain it |

|

Dispute resolution |

How the partners will resolve problems (e.g., mediation or other process) |

This isn’t an all-inclusive list, but it provides an idea of what most partnership agreements cover.

Note that partnerships are tax-reporting entities (not tax-paying). It’s required to file Form 1065 annually to provide information to the IRS about business profits and losses. However, the business doesn't pay taxes to the government.

Instead, profits and losses pass through to the owners. Each owner must fill out a tax return and include details about their percentage share of the profit (based on the partnership agreement). They then pay taxes on their portion of the profits or report a loss.

Partnerships aren’t difficult to form, but require detailed agreements that are best done with the help of an attorney.

The cost to start a business partnership depends on several factors like:

- Location/state of registration.

- Number of partners involved.

- Type of partnership (LP vs LLP).

- Complexity of partnership agreement.

For example, registration fees can range from around $200 for an LP in Delaware to $1,061 for an LLP in Florida. Many states also require annual renewal fees, which can be as high as $820.

Examples of partnerships include medical, legal, and dental practices.

Example: Digital Content Solutions

Another freelancer and I considered forming a partnership to combine our expertise. I‘d handle B2B SaaS content strategy and writing while they’d manage SEO and content distribution, and we would have split profits 60-40 based on workload, with me as the majority partner.

However, we opted against this structure due to shared liability concerns. If one partner made a mistake with a client's product messaging or SEO strategy, both of us would be personally liable.

Free Business Plan Template

The essential document for starting a business -- custom built for your needs.

- Outline your idea.

- Pitch to investors.

- Secure funding.

- Get to work!

Download Free

All fields are required.

Form not available

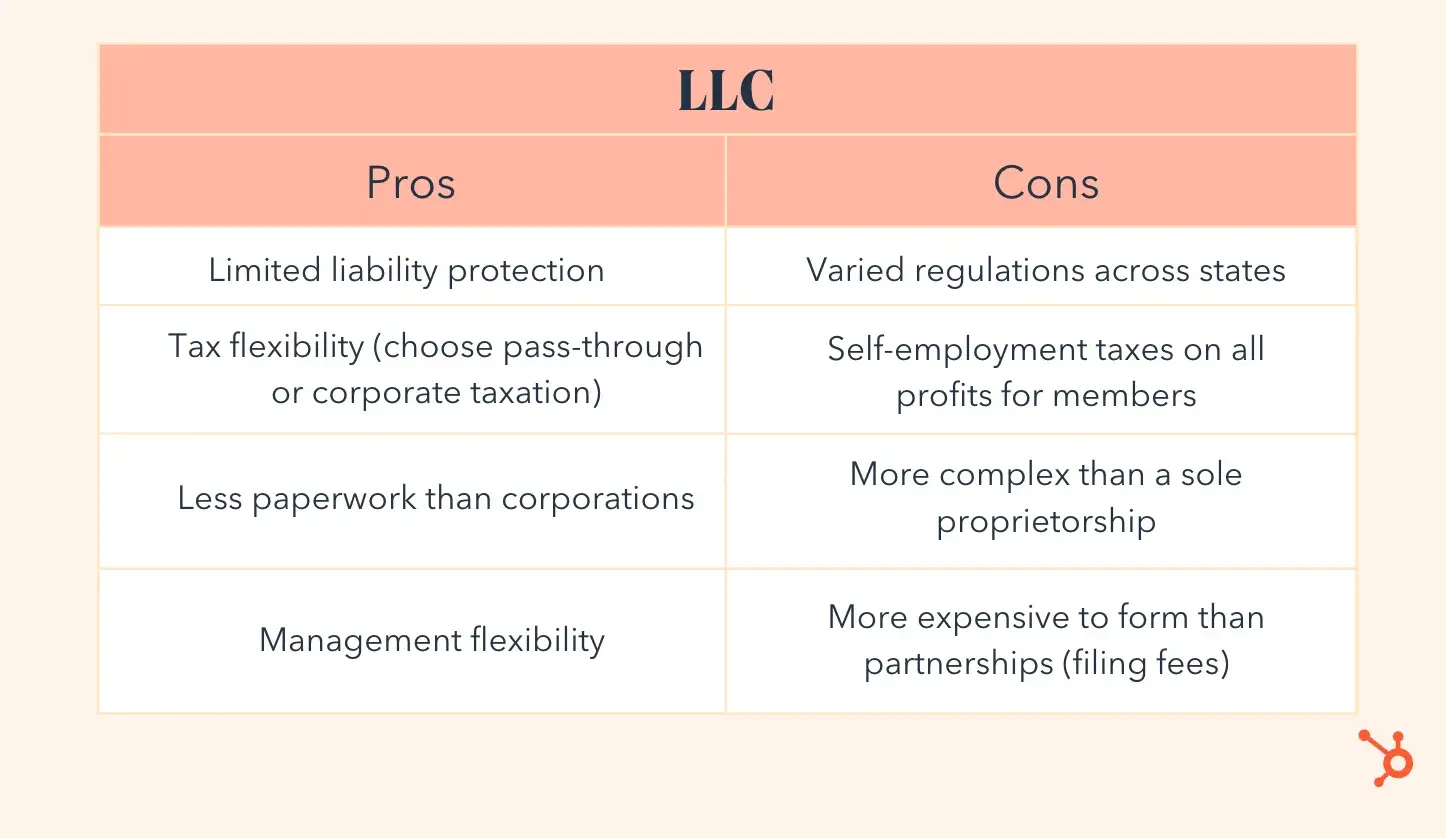

3. Limited Liability Company

A limited liability company, or LLC, is a mix of corporate, sole proprietorship, and partnership legal business structures. It provides liability protection to safeguard your personal possessions from business debts.

LLCs can have one or more members, like a partnership. However, some states require the business to dissolve when someone leaves the company. You can then re-form the company under the same or a different business structure.

If you plan to sell the company one day, include a clause in the agreement about buying, selling, and transferring ownership of the LLC.

An LLC is a tax-reporting entity and must file an informational tax return. However, it pays no taxes to the IRS as its business income passes through the company to the LLC members. Each member files an individual tax return to report their share of profits or losses. This can prevent double taxation (paying corporate taxes on the profits, while also paying personal income tax on your owner’s salary).

However, since LLC members are self-employed, they pay self-employment tax contributions for Medicare and Social Security.

Note:

- If you’re the only LLC member, you can report business expenses using Form 1040 Schedule C, E, or F.

- If there are two or more LLC members, each must file a partnership return using Form 1065.

Each LLC member’s profit share is taxable income, including undistributed profits.

The cost to form an LLC depends on the state but can range between $100 and $800. In addition, if you are doing business in your state, it is best to form an LLC in that state. Otherwise, if you form an LLC in another state, you will have to pay your fees twice.

You must also have articles of organization (certification of formation) before establishing the business.

Some states require an LLC operating agreement outlining:

- Profit and loss sharing.

- Buy-sell provisions.

- Member voting power.

- Ownership interest per member.

- Rights and responsibilities of each member.

LLC is an ideal business structure for medium-risk companies. It separates your business and personal finances, since you’ll need a separate LLC bank account to run your business (this holds true for all business structures except for sole proprietorship).

Examples of LLCs include real estate companies, law firms, accounting firms, and consulting businesses.

Example: My Current LLC Structure

I operate my B2B SaaS content consulting business as an LLC, which protects my personal assets while maintaining operational flexibility.

This structure works perfectly for my high-value consulting work with software companies, where a single messaging mistake could potentially impact a client's product launch.

I can also easily bring on subcontractors for larger projects, scale my services, and maintain professional credibility with enterprise clients who prefer working with LLCs over sole proprietors.

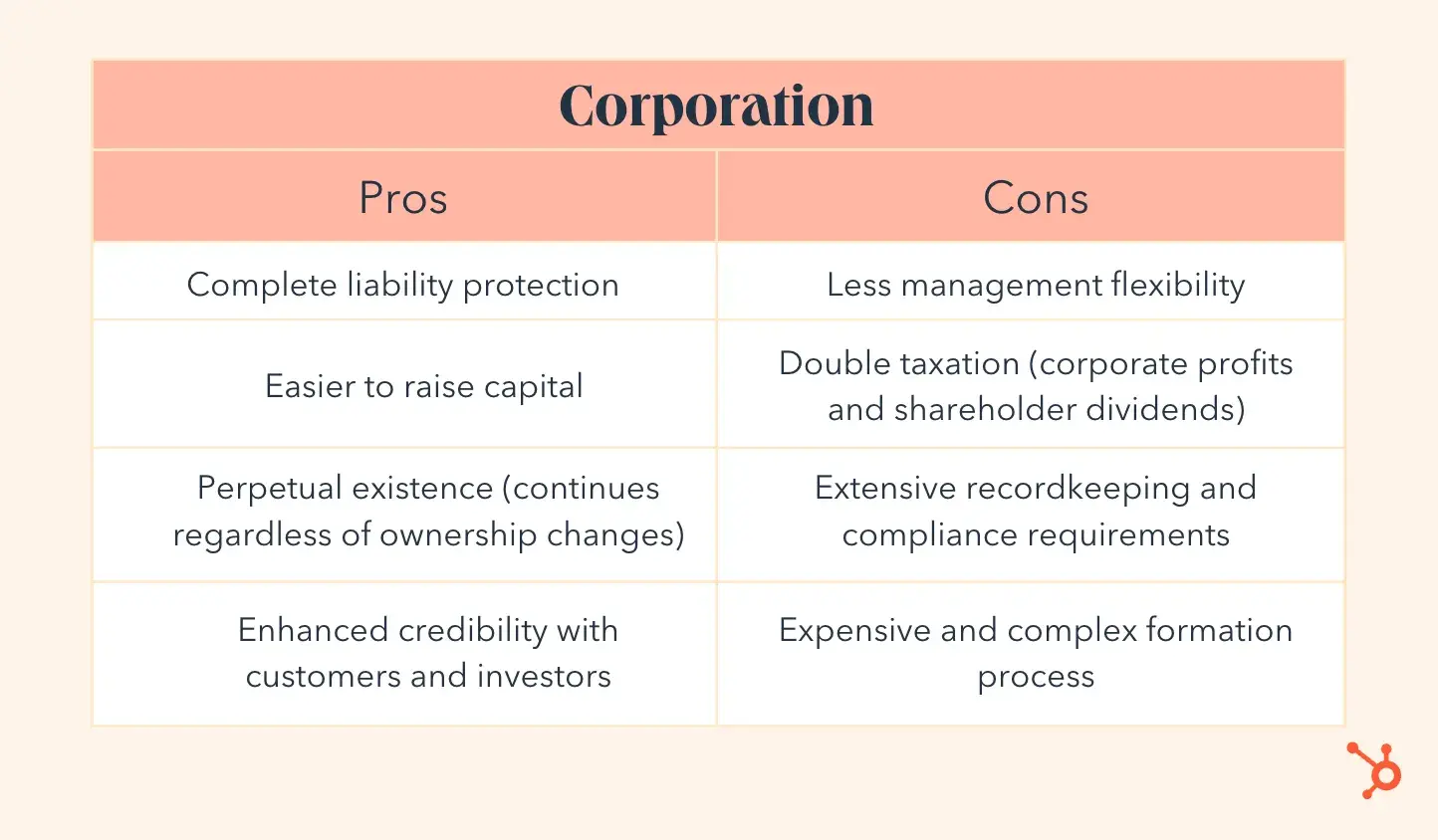

4. Corporation

A corporation, or C-corp, is independent of the people who own and run it (shareholders). As a shareholder, you own portions (shares) of the corporation, giving you partial ownership rights.

Shareholder benefits include:

- More shares = greater voting power in company decisions.

- Receive dividends (share of post-tax profits).

- Dividends only taxed upon distribution to shareholders.

- Personal assets protected from business liabilities.

- Shares can be passed on after death according to formal documents.

A corporation is considered a separate legal person — it has its own assets and liabilities. Therefore, it can do things separate from its owners, such as enter into contracts, sue and be sued, and pay taxes. Its structure even protects shareholders’ personal assets from business liabilities and debts.

It’s similar to a partnership, except corporations are owned by shareholders who elect directors to oversee the company. The board of directors then hires managers to run the business. So it’s an attractive option for investors who want to earn from the company, but don’t want to work “in” the business.

There are two types of corporations: C-Corporations and S-Corporations. Here are some of their differences.

|

Feature |

C-Corporation |

S-Corporation |

|

Tax form |

Form 1120 |

Form 1120S |

|

Who pays taxes |

Corporation pays tax on profits, AND shareholders pay tax on dividends |

Only shareholders pay tax on their share of profits |

|

Tax treatment |

Double taxation |

Pass-through taxation |

It’s common for sole proprietors and LLC businesses to elect to be taxed as S-corporations to save on taxes. But it’s only worth it if you earn at least $75k a year.

For example, your business generates $100k in earnings per year — and instead of the entire amount passing onto you like a regular LLC member, you could split the $100k by paying yourself a salary of $50k and taking the rest as dividends. You’ll pay $7,650 in self-employment tax (or 15.3%) for your pass-through income — not the dividends — saving you $7,650 compared with getting all $100k as a pass-through.

Although forming a corporation is the most complex, it’s affordable, costing between $50 and $200.

Examples of corporations include social media companies, software companies, and grocery chains.

Example: My B2B SaaS Clients like HubSpot

Most of my clients, including HubSpot, operate as corporations. This structure makes sense for SaaS companies because they often need to raise significant capital, have multiple shareholders, and plan for rapid growth.

As a content consultant, I work directly with their marketing teams but understand that major decisions go through their board of directors.

The corporate structure helps these companies manage complex operations across multiple products, attract top talent with stock options, and maintain the professional image needed for enterprise sales.

Think Bigger Than Your Current Situation

Writing this piece reminded me of all the conversations I‘ve had with fellow consultants who rushed into choosing a business structure without proper research. I’ve seen talented writers get stuck in partnerships that limited their growth and others who outgrew their sole proprietorships but waited too long to make a change.

There's no one-size-fits-all solution — understand where you want your business to go and build the right foundation to get there.

While the paperwork and legal considerations might seem overwhelming at first, investing time in this decision early on saves considerable headaches down the road.

Free Business Plan Template

The essential document for starting a business -- custom built for your needs.

- Outline your idea.

- Pitch to investors.

- Secure funding.

- Get to work!

Download Free

All fields are required.

Form not available

Business Acumen

![Business Ethics — Why They Matter and How Your Company Can Get it Right [+Expert Tips]](https://53.fs1.hubspotusercontent-na1.net/hubfs/53/business-ethics-1-20250224-5750570.webp)

.jpg)